By: Robert J. Nahoum

What are judgment exemptions in New York?

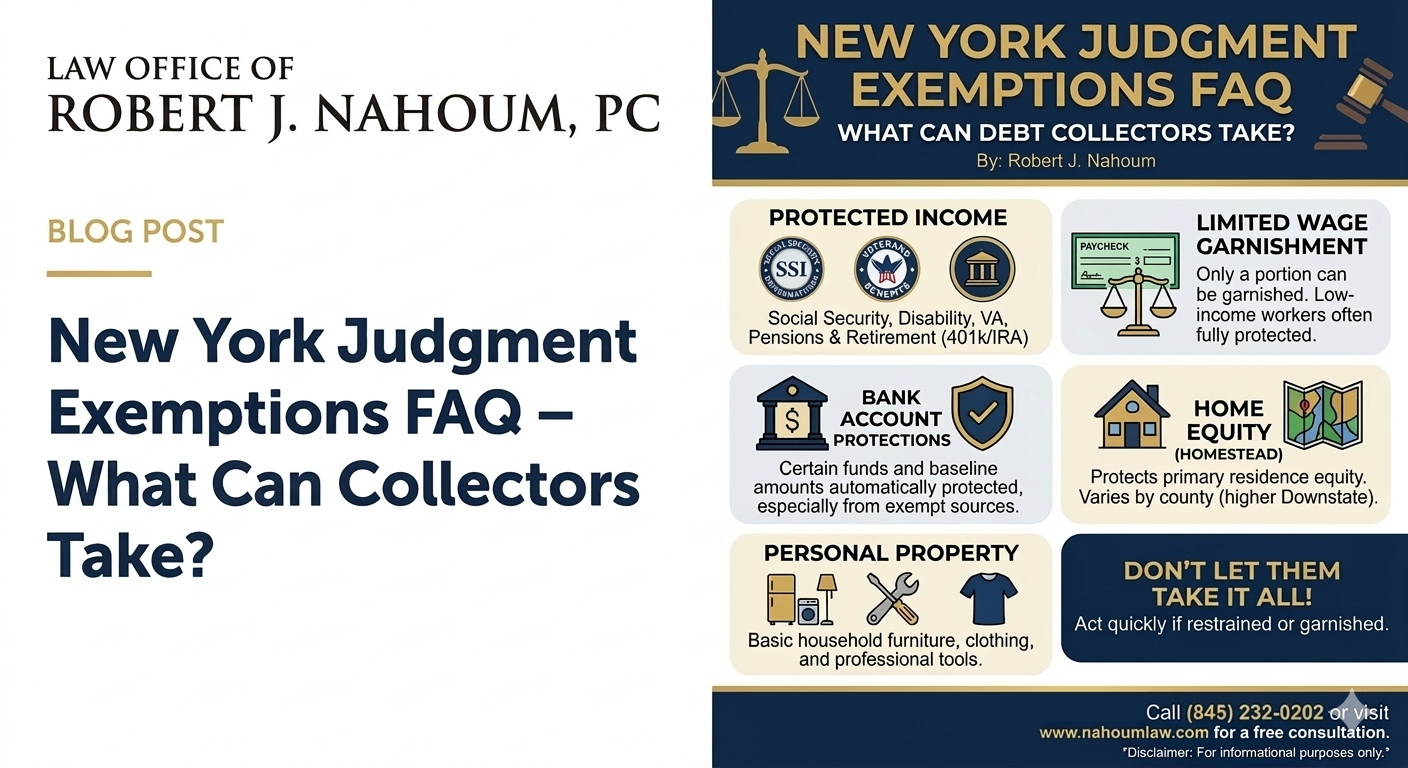

Judgment exemptions are protections in New York and federal law that keep certain income and property safe from most judgment creditors’ reach. These rules limit what debt collectors can take through wage garnishments, bank restraints, and property levies, even after they win a judgment against you.

If a debt collector gets a judgment, can they take everything I own?

No. A judgment is not a license for a debt collector to take everything. Exemption laws protect specific types of income (like Social Security and unemployment) and certain property (like some home equity and basic household items). If most of what you have is exempt, you may effectively be “judgment proof” even though a judgment exists.

What income is protected from judgment creditors?

Common examples of exempt income include:

- Social Security retirement and disability benefits

- Supplemental Security Income (SSI)

- Veterans’ benefits

- Public assistance (welfare)

- Unemployment insurance

- Workers’ compensation

- Many pensions and retirement accounts (such as 401(k)s and IRAs, subject to limits)

Private judgment creditors generally cannot take this income. If your only income comes from these sources, you are usually well protected from wage garnishments.

Are my wages completely exempt from garnishment?

Not completely, but New York strictly limits how much of your paycheck can be garnished. Only a portion of your wages can be taken, and low‑income workers are often fully protected from garnishment. The exact amount depends on your earnings and current statutory thresholds.

Are funds in my bank account exempt?

Some are, and some are not. New York law protects certain funds in your bank account, especially when they come from exempt sources. Important points:

- Social Security, SSI, VA benefits, and public assistance retain their exempt status when directly deposited.

- New York law automatically protects a baseline amount in accounts that contain exempt funds.

- Additional protections may apply to certain government-related emergency payments and some tax refunds, subject to the rules in place at the time.

The problem is that banks and debt collectors often treat accounts as non‑exempt, especially when exempt and non‑exempt money are mixed. You may have to actively assert your exemptions and challenge an improper restraint.

What is the New York homestead exemption?

The homestead exemption protects a portion of the equity in your primary residence from most judgment creditors. Key features:

- It only applies to your principal residence, not an investment or vacation property.

- The amount of protected equity depends on the county where you live. Downstate counties (including the five boroughs, Rockland, Westchester, Nassau, Suffolk, and some neighbors) have higher exemption amounts.

- If you co‑own your home with your spouse, you may be able to double the exemption.

The homestead exemption does not stop a mortgage foreclosure or collection on debts specifically secured by the home, but it can make a forced sale for a consumer judgment impractical or impossible.

Can a judgment creditor force the sale of my home?

Sometimes, but often not. Whether a creditor can realistically force a sale depends on:

- How much your home is worth

- How much you owe on mortgages or liens

- How much of your equity is covered by the homestead exemption in your county

If most or all of your equity is exempt, a forced sale is usually off the table. A careful analysis of your property and the exemption rules is essential before any creditor can try to reach your home.

What personal property is exempt from judgment enforcement?

New York exempts certain personal property so a judgment does not leave you unable to live or work. Depending on current statutory limits, examples include:

- Basic household furniture and appliances up to specific values

- Necessary clothing and personal effects

- Certain tools and equipment you need for your trade or profession

- Portions of insurance and annuity proceeds

- Portions of personal injury or wrongful death recoveries

These protections are technical and value‑limited, so it is important to review your specific situation with a lawyer before assuming an item is fully exempt.

What does it mean to be “judgment proof”?

You are “judgment proof” when, even if a creditor has a judgment, they cannot practically collect because your income and assets are exempt or minimal. Typical examples include:

- Seniors living only on Social Security

- Disabled individuals receiving SSI or SSDI and owning little property

- Low‑income workers whose wages fall below garnishment thresholds and who do not own real estate

Being judgment proof today does not mean you will always be judgment proof. If your financial circumstances improve, creditors may try again to enforce the judgment.

What should I do if my wages are being garnished or my bank account is frozen?

Act quickly. Steps you should consider:

- Gather pay stubs, bank statements, and notices from the marshal, sheriff, or creditor.

- Identify whether the money being taken comes from exempt sources.

- Contact an experienced consumer protection lawyer to help you file exemption claim forms or court motions to release exempt funds and stop improper garnishments.

At The Law Offices of Robert J. Nahoum, P.C., we regularly help consumers challenge improper garnishments and bank restraints and seek the return of wrongfully taken funds.

How can a debt collection defense lawyer help me with exemptions?

A knowledgeable debt collection defense lawyer can:

- Analyze your income and assets to determine what is exempt

- Explain the risks of wage garnishment, bank restraint, or property levy in your specific case

- Prepare and file exemption claim forms, motions to vacate default judgments, and motions to release restrained funds

- Negotiate with creditors to reduce or resolve the judgment when appropriate

- Make sure you respond properly to information subpoenas and restraining notices without giving up rights

How do I contact The Law Offices of Robert J. Nahoum, P.C.?

If you have been sued by a debt collector, received a default judgment notice, or discovered that your wages or bank account are being hit by a judgment creditor, we can help.

Contact The Law Offices of Robert J. Nahoum, P.C. for a free consultation:

- Phone: (845) 232‑0202

- Website: https://www.nahoumlaw.com

Disclaimer: This FAQ is for general informational purposes only and is not legal advice. Exemption laws change, and how they apply depends on your specific facts. You should consult with an attorney about your situation before taking any action.