By: Robert J. Nahoum

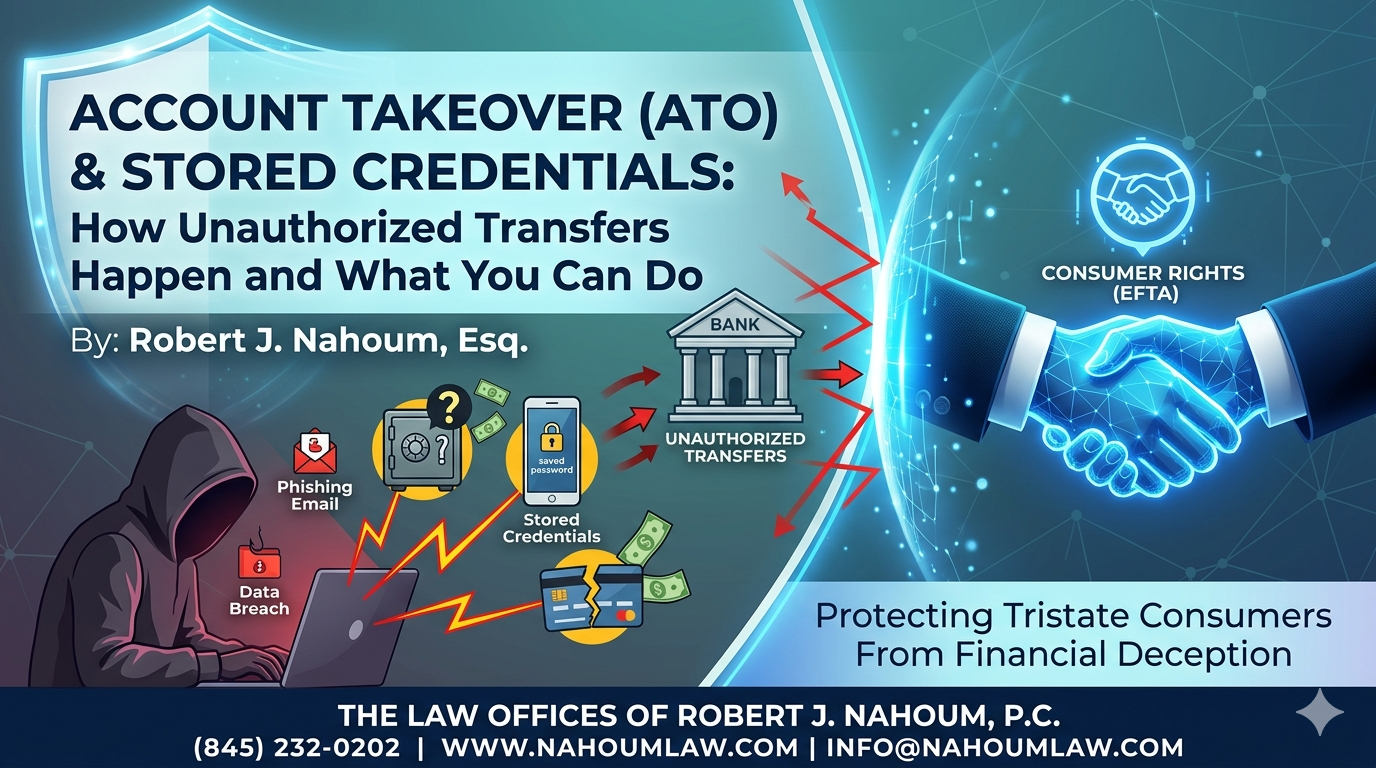

Account takeover (ATO) is one of the fastest-growing forms of financial fraud, and it often leads directly to unauthorized electronic funds transfers from your bank account, credit card, or payment apps. Many consumers are surprised to learn that these incidents frequently involve “stored credentials”, saved usernames, passwords, or payment information, — rather than traditional hacking in the dramatic sense.

If you have noticed unfamiliar withdrawals, transfers, or charges, understanding how these schemes work is the first step toward protecting your rights.

What Is Account Takeover (ATO)?

Account takeover occurs when a third party gains access to your financial account — such as a bank account, credit card, or payment platform — and uses it without your authorization.

This is often done through:

- Phishing emails or fake websites that trick you into entering login credentials

- Data breaches where your username and password are exposed

- Malware or spyware installed on your device

- Credential stuffing (using reused passwords across multiple sites)

Once access is obtained, the fraudster can initiate transfers, change account settings, or link your account to external payment systems.

What Are “Stored Credentials”?

Stored credentials refer to payment or login information saved by a merchant, app, or browser for future use. This includes:

- Saved credit or debit card numbers

- Bank account information linked to apps (e.g., ACH authorization)

- Auto-fill login credentials in browsers or password managers

- Recurring billing authorizations

While convenient, stored credentials can become a major vulnerability if accessed by unauthorized parties.

How ATO and Stored Credentials Lead to Unauthorized Fund Transfers

In many cases, fraud does not involve breaking into your bank directly. Instead, it exploits weak points in the broader ecosystem of stored credentials.

Here are common scenarios:

- A fraudster accesses your email, resets your bank password, and initiates transfers

- Your credentials from a data breach are reused to access a financial app

- A compromised merchant account is used to trigger recurring charges

- A payment app linked to your bank account is accessed and used to send funds

- Browser-saved card information is used for unauthorized purchases

Because the transactions may appear “authorized” on the surface (i.e., using correct credentials), financial institutions sometimes deny claims — even when the consumer did not actually authorize the transaction.

Your Rights Under Federal Law

Consumers are protected under federal laws such as the Electronic Fund Transfer Act (EFTA), which governs unauthorized electronic transfers from bank accounts.

Key protections include:

- Limited liability if you report unauthorized transfers promptly

- The right to a timely investigation by your financial institution

- The right to reimbursement for unauthorized transactions in many cases

However, disputes often arise when banks claim:

- The transaction was authorized because correct credentials were used

- The consumer was negligent in safeguarding credentials

- The transaction falls outside EFTA protections

These issues frequently require legal analysis, especially in complex ATO cases.

Common Red Flags of ATO-Related Fraud

Be alert to these warning signs:

- Unexpected password reset emails

- Notifications of logins from unfamiliar devices or locations

- New linked accounts or payment methods you did not add

- Small “test” transactions followed by larger withdrawals

- Locked accounts or changed contact information

Acting quickly can significantly reduce financial loss and improve your legal position.

What To Do If You Are a Victim

If you suspect account takeover or unauthorized transfers:

- Immediately notify your bank or financial institution

- Change all passwords, especially for email and financial accounts

- Enable multi-factor authentication where available

- Document all unauthorized transactions and communications

- File a written dispute under the EFTA

Final Thoughts

Account takeover cases involving stored credentials are increasingly common and often misunderstood. Financial institutions may attempt to shift responsibility onto consumers, but the law provides important protections — especially when transfers were not truly authorized.

Understanding how these schemes operate can help you both prevent fraud and respond effectively if it occurs.

Protecting Consumers Against Financial Deception

If you need help recovering money lost to an impersonation scam, contact us today to see what we can do for you. With offices located in Brooklyn and the Hudson Valey, the Law Offices of Robert J. Nahoum represents consumers in cases throughout the Tristate area including New Jersey.

The Law Offices of Robert J. Nahoum, P.C

(845) 232-0202

www.nahoumlaw.com

info@nahoumlaw.com

Disclaimer: This blog post is for informational purposes only and does not constitute legal advice. Laws and regulations are subject to change. Please consult with an attorney for advice regarding your specific situation.