By: Robert J. Nahoum

If you have purchased a car in the last several years, chances are you were asked to “sign” documents electronically—either on a tablet like an iPad or on a small signature capture pad. While these technologies are marketed as convenient and modern, they can also be used in ways that leave consumers in the dark about what they are actually agreeing to.

As a consumer protection attorney, I regularly represent clients who were misled during the car-buying process. Understanding how these systems work—and how they can be abused—is critical.

The Two Common Digital Signing Methods

Auto dealers typically use one of two electronic signature systems:

- Tablets (such as iPads or touchscreen monitors)

- Signature capture devices (small pads that only display a signature box)

At first glance, both methods seem similar. You sign electronically, and the dealer processes your paperwork digitally. But the experience—and the risks—can be very different.

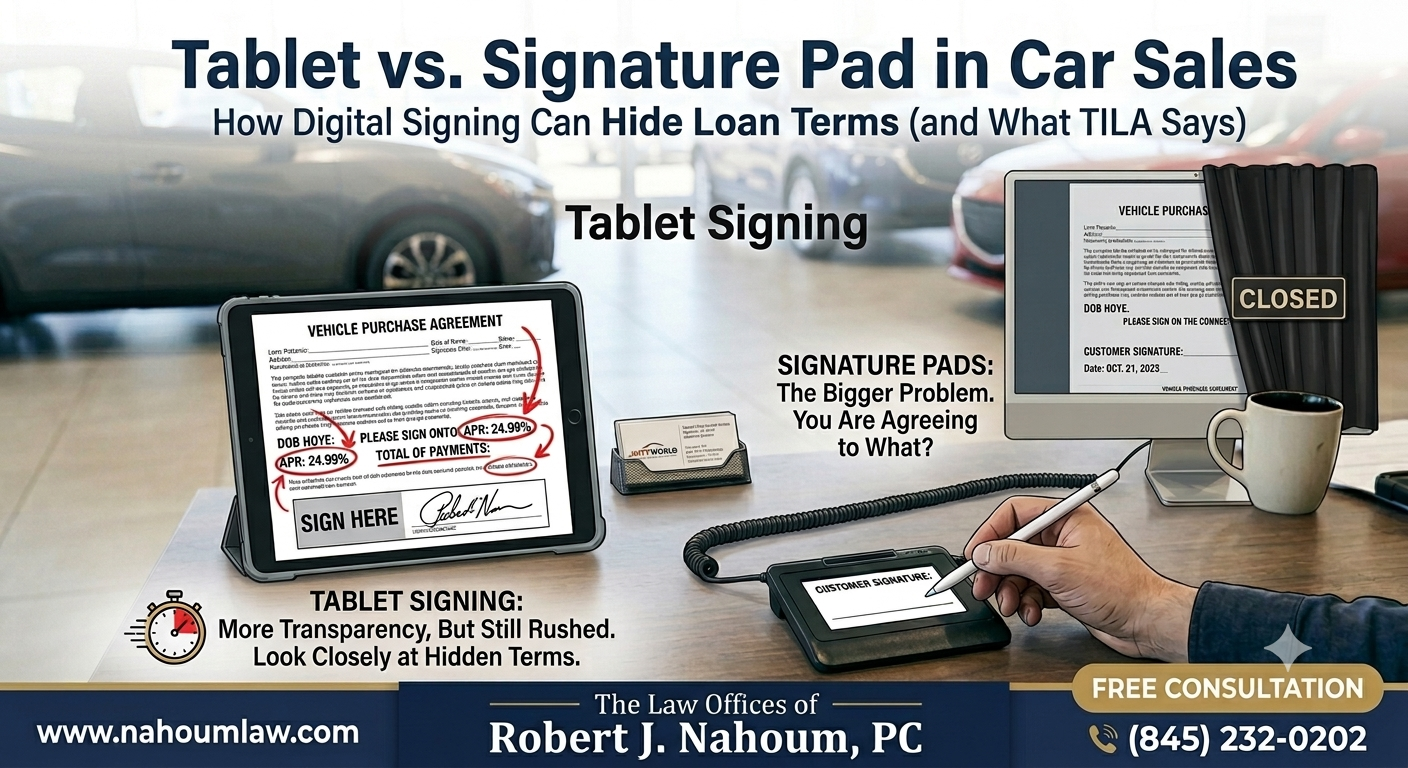

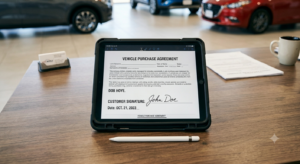

Tablet Signing: More Transparency, But Still Risky

When you sign on a tablet, you are usually shown the full document on the screen. In theory, this hands control over the document to you and allows you to scroll, read, and review the terms before signing.

However, in practice:

- Sales staff often rush consumers through the process

- Key financial terms may not be clearly highlighted

- Consumers are discouraged from carefully reviewing documents

- Documents can be flipped quickly, with little explanation

Even though the full contract may technically be visible, the speed and pressure of the transaction can prevent meaningful review.

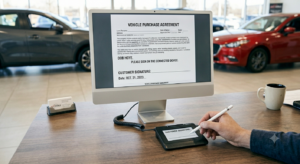

Signature Pads: The Bigger Problem

Signature capture devices are far more concerning.

These devices typically:

- Show only a blank box where you sign

- Do not display the full contract or any terms

- Capture your signature separately from the document

After you sign, your signature is electronically applied to documents that you may never have seen.

This creates a serious risk: consumers may unknowingly “agree” to loan terms, fees, or add-ons that were never disclosed.

How Dealers Use These Tools to Hide Terms

In fraudulent or deceptive transactions, these technologies can be used to:

- Insert higher interest rates than originally discussed

- Add unwanted products (extended warranties, GAP insurance, service plans)

- Change loan durations or payment amounts

- Inflate the vehicle sale price

- Include hidden fees or inflated charges

Because the consumer never fully reviewed the final contract—or was rushed through it—these discrepancies often go unnoticed until much later.

Why This May Violate the Truth in Lending Act (TILA)

The Truth in Lending Act (TILA) requires that lenders clearly and conspicuously disclose key credit terms before a consumer becomes obligated.

This includes:

- The annual percentage rate (APR)

- The finance charge

- The total amount financed

- The total of payments

If a dealer uses electronic signing in a way that prevents a consumer from meaningfully reviewing these disclosures, it may constitute a violation of TILA.

For example:

- If disclosures are not actually shown before signing

- If the consumer is rushed or misled about the terms

- If the signed documents differ from what was presented

These situations can give rise to legal claims.

Electronic Signatures Are Legal—But Not a Free Pass

It is important to understand that electronic signatures themselves are legal under federal law (E-SIGN Act). Dealers are allowed to use tablets and signature pads.

However, legality of the technology does not excuse deceptive practices.

The key issue is whether the consumer had a fair opportunity to review and understand the terms before signing.

What Consumers Should Watch For

If you are buying a car, take these precautions:

- Ask to see every document in full before signing

- Do not sign on a device that does not display the contract

- Request printed copies immediately

- Take your time—do not let anyone rush you

- Compare the final contract to what you were told verbally

If something feels off, it probably is.

When to Speak With a Lawyer

If you discover after the fact that your loan terms are different from what you agreed to, you may have legal options.

Common warning signs include:

- Higher monthly payments than expected

- Unexpected add-ons or fees

- Interest rates that differ from what was promised

- Missing or altered documents

At The Law Offices of Robert J. Nahoum, P.C., we represent New York and New Jersey consumers who have been ripped off by dishonest auto dealers. If your deal doesn’t match what was promised, you have rights—and we can help you enforce them.

For a free consultation about an auto‑fraud or deceptive‑sales issue, contact us at our Hudson Valley office or our Brooklyn location.

📞 Call (845) 232‑0202 or visit our contact page: www.nahoumlaw.com/contact