By: Robert J. Nahoum

Discovering an unauthorized transfer from your bank account is alarming. But your financial protection under the Electronic Fund Transfer Act (EFTA) depends critically on when you report it.

The EFTA establishes two essential deadlines: the 2-day rule and the 60-day rule. Understanding both, and how they work together, can mean the difference between losing $50 or losing thousands.

At Nahoum Law, we represent consumers victimized by unauthorized electronic funds transfers. We frequently see bank denials based on confusing or misapplying these deadlines. Learn more about your rights on our EFTA lawyer page.

The 2-Day Rule: Your $50 Liability Protection

The 2-day rule is your most important protection. It applies when you discover any unauthorized transfer, whether you find it on your monthly statement, through account monitoring, or any other means.

What the Rule Actually Says

If you notify your bank within 2 business days of discovering the unauthorized transaction:

- Your liability is capped at $50 maximum

- This applies even if the thief transferred $5,000 or more

- You get back all money beyond $50

If you notify after 2 business days but within 60 days:

- Your potential liability increases to $500 maximum

- You still recover most of your money, but you absorb more loss

Example: Someone steals your debit card number and drains $3,000 from your account. You discover this on your monthly statement:

- Report within 2 business days of seeing it: You lose only $50

- Report 5 days after seeing it (but within 60 days): You could lose up to $500

- Report after 60 days: You could lose everything transferred after day 60

The key is discovery: The 2-day clock starts when you find the problem, not when it happened.

The 60-Day Rule: Your Statement Review Deadline

The 60-day rule is a separate requirement focused on your periodic bank statement.

What the Rule Actually Says

You must report unauthorized transfers appearing on your statement within 60 days of when the bank transmitted that statement:

- If you report within 60 days: You’re protected for all unauthorized transfers on that statement

- If you report after 60 days: You become liable for any unauthorized transfers occurring after the 60-day period that the bank can prove wouldn’t have happened had you reported sooner

This is where liability becomes unlimited, not just $500. If you miss the 60-day deadline and the bank can show that subsequent fraud would have been prevented by timely reporting, you bear all those losses.

Example: Your January 15 statement shows an unauthorized $200 charge on January 10:

- Report by March 15 (60 days from statement date): You get the $200 back

- Report April 1 (after 60 days): If another $2,000 was stolen in February/March that would have been prevented, you might be liable for that $2,000

How the Two Rules Work Together

These deadlines function as dual protections:

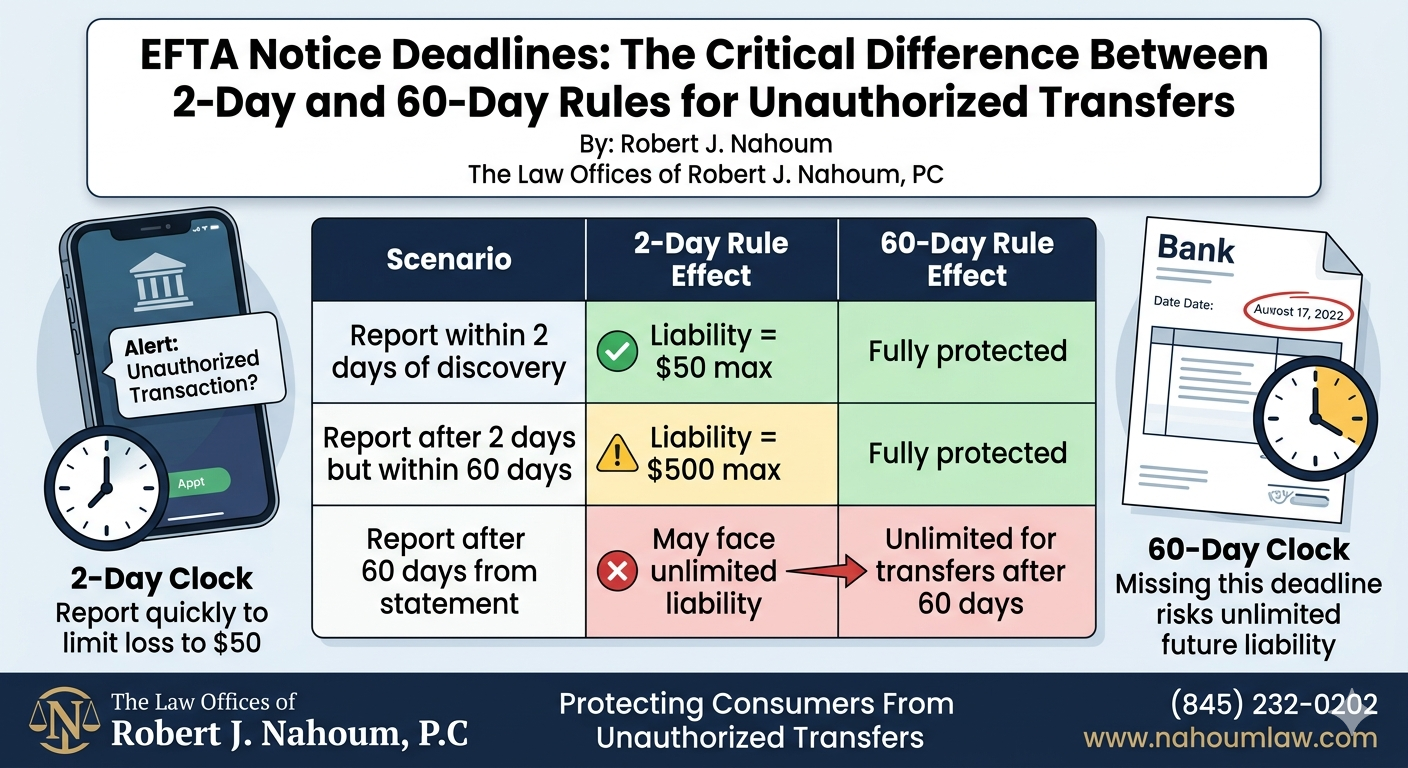

| Scenario | 2-Day Rule Effect | 60-Day Rule Effect |

| Report within 2 days of discovery | Liability = $50 max | Fully protected |

| Report after 2 days but within 60 days | Liability = $500 max | Fully protected |

| Report after 60 days from statement | May face unlimited liability | Unlimited for transfers after 60 days |

The 2-day rule determines your maximum liability cap ($50 vs. $500). The 60-day rule determines whether you face unlimited liability for future fraud.

Best practice: Report within 2 business days of discovering any unauthorized transaction to limit losses to $50 while staying within the 60-day window.

Common Misconceptions That Cost Consumers

We regularly see these dangerous misunderstandings:

- “The 2-day rule only applies to lost cards” — False. The 2-day rule applies to any discovered unauthorized transfer, including those on your statement

- “60 days starts when the transaction occurred” — False. The 60-day clock starts when the bank transmits the statement containing the transaction

- “If I miss 2 days, I’m liable for everything” — False. You’re liable for up to $500 if you report within 60 days, but unlimited only if you miss 60 days

- “ACH transfers don’t count” — False. The law covers all electronic fund transfers from consumer accounts, including ACH debits and wire transfers

What Banks Must Do When You Report

Once you notify your bank of unauthorized transfers:

- Investigation timeline: The bank generally has 10 business days to investigate (may extend to 20 days in certain cases)

- Temporary credit: If the bank can’t complete its investigation within 10/20 days, it must issue a temporary credit to your account (minus up to $50)

- Error correction: If the bank determines an error occurred, it must correct it within 1 business day

- Findings notice: The bank must report its findings to you within 3 business days after deciding

Banks sometimes fail these obligations. If your bank denied your claim or refused to investigate properly, you may have legal recourse.

When the 2-Day Rule Applies to Lost Cards Specifically

There’s one situation where the 2-day rule has a special trigger:

If your physical debit card is lost or stolen:

- The 2-day clock starts when you learn of the loss/theft, not when you see unauthorized transactions

- Report within 2 days: $50 maximum liability

- Report after 2 days: Up to $500 liability

This differs from statement errors because the clock starts earlier (at loss notification, not transaction discovery).

What to Do If You Spot Unauthorized Activity

Immediate action protects you:

- Call your bank immediately to report unauthorized transactions

- Follow up in writing within 2 business days to create a paper record

- Keep copies of all communications and periodic statements

- Request written confirmation that your dispute has been filed

- Monitor your account closely for additional unauthorized transfers

Even if you’re uncertain about deadlines, reporting quickly protects you under both the 2-day and 60-day rules.

When Banks Misapply These Rules

Banks frequently deny legitimate claims by misapplying notice deadlines:

- Claiming you missed 2 days when you actually reported within 2 business days of discovery

- Starting the 60-day clock from the transaction date instead of the statement transmission date

- Failing to provide temporary credits during investigation as required by Regulation E

- Not proving that subsequent fraud “would not have occurred” had you reported earlier (required for unlimited liability)

- Ignoring that the 2-day rule applies to all unauthorized transfers, not just lost cards

If your bank denied your unauthorized transfer claim, you may have grounds for legal action under the EFTA. The law provides for statutory damages, and banks must follow investigation and credit obligations.

Protecting Consumers From Unauthorized Transfers

If you need help recovering money lost to unauthorized electronic fund transfers, contact us today to see what we can do for you. With offices located in Brooklyn and the Hudson Valey, the Law Offices of Robert J. Nahoum represents consumers in cases throughout the Tristate area including New Jersey.

The Law Offices of Robert J. Nahoum, P.C

(845) 232-0202

www.nahoumlaw.com

info@nahoumlaw.com

Disclaimer: This blog post is for informational purposes only and does not constitute legal advice. Laws and regulations are subject to change. Please consult with an attorney for advice regarding your specific situation.