By: Robert J. Nahoum

What Is New York City’s New SHIELD Rule?

New York City has adopted a new “Stopping Harassment and Intimidation and Ensuring Lawful Debt (SHIELD) Collection Rule” that significantly strengthens protections for people facing debt collection in the five boroughs. It goes beyond the federal Fair Debt Collection Practices Act (FDCPA) by adding stricter limits on communications, broader rights to dispute and verify debts, and special protections for medical and time‑barred debts.

The rule is enforced by the New York City Department of Consumer and Worker Protection (DCWP), which licenses and supervises debt collection agencies in the city. It applies to debt collectors, debt buyers, collection law firms, and, in certain situations, even original creditors trying to collect consumer debts from New York City residents.

For a deeper look at how debt collection works in New York and how lawsuits get filed, you can also review my FAQ on how to respond to a debt collection lawsuit in New York.

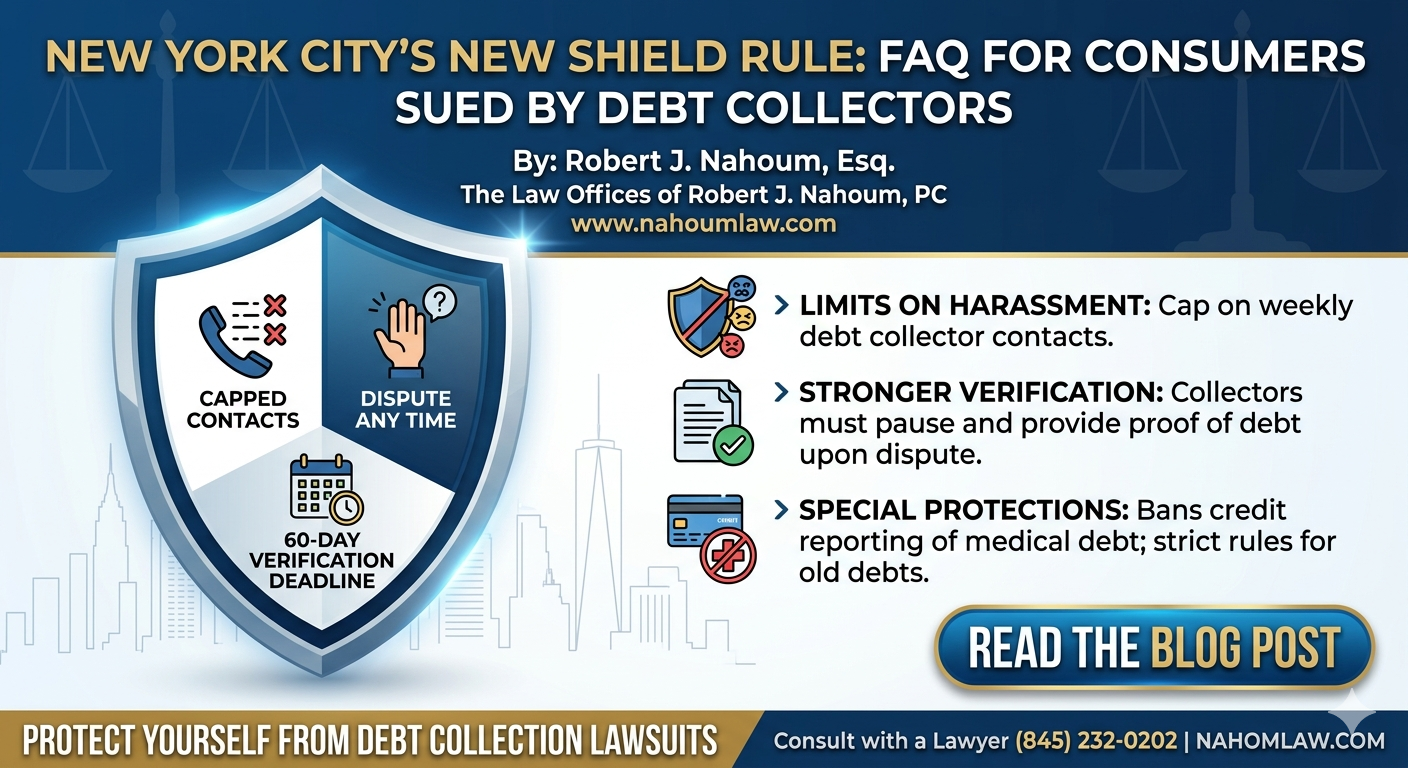

How Does the SHIELD Rule Protect Consumers?

The SHIELD Rule introduces multiple layers of protection for New York City consumers dealing with debt collectors. Key features include:

- Limits on collector contacts: Collectors are capped at a small number of contacts (such as calls or messages) per seven‑day period, aimed at preventing harassment and repeated intimidation.

- Dispute rights at any time: You can dispute a debt and request verification at any point in the collection lifecycle.

- Stronger verification obligations: When you dispute or request verification, collectors must provide documentation showing the debt is yours, in the correct amount, and legally collectible, and they must pause certain collection activities until they comply.

- 60‑day verification deadline: The rule sets a 60‑day limit for collectors to provide supporting documentation after you dispute the debt; a default judgment by itself is not enough to verify the debt. If they do not comply, third‑party collectors and debt buyers can lose the right to continue collection on that debt.

- Special protections for medical debt: Collectors are prohibited from furnishing information about medical debt to consumer reporting agencies and must follow additional rules when collecting medical bills.

- Time‑barred debt disclosures: Before trying to collect on a time‑barred debt (where the statute of limitations has expired), collectors must send a mandated written notice and wait 14 days before further collection efforts, including warning that paying may restart the statute of limitations in some cases.

- Coverage of original creditors in some situations: Certain original creditors become subject to the rule when they pursue collection after accelerating a debt, demanding payment in full, or stopping periodic billing statements.

For a practical explanation of documentation and substantiation of debts, including what collectors must provide and how collection must pause while they do so, see my article “What It Means to Demand Substantiation of a Debt in New York”.

FAQ: Common Questions About the SHIELD Rule

Does the SHIELD Rule apply if I live in New York City but the collector is located elsewhere?

Yes. The SHIELD Rule is focused on protecting New York City consumers, so out‑of‑state collectors and law firms attempting to collect from NYC residents must comply when they are subject to New York City’s licensing and regulations.

Can I dispute my debt even if I’ve been getting collection calls for months?

Yes. One of the most important aspects of the SHIELD Rule is that you can dispute a debt and request verification at any time during the collection process. Once you dispute, the collector must pause certain collection activities and obtain adequate documentation before resuming.

What happens if the collector does not send verification within 60 days?

If a third‑party debt collector or debt buyer does not provide the required supporting documentation within 60 days of your dispute or verification request, they can lose the right to continue collection efforts on that debt under the SHIELD Rule. A default judgment alone is specifically not enough to count as verification.

Are there special rules for medical debt?

Yes. Collectors face enhanced requirements when collecting medical debt, including a prohibition on furnishing medical debt to consumer reporting agencies and heightened scrutiny from regulators. This is designed to prevent long‑term credit damage from medical bills and to ensure collectors handle these sensitive obligations lawfully.

Can I sue directly under the SHIELD Rule?

The SHIELD Rule does not itself create a new private right of action, meaning you generally cannot sue solely “under SHIELD.” However, violations can still be powerful evidence in cases under existing federal and state consumer protection laws, and DCWP can enforce the rule through investigations, penalties, and injunctions.

For more on how violations of debt collection rules can help your defense or support claims against collectors, see my New York debt collection lawsuit FAQ

Action Plan: What Should Consumers Do If They Need SHIELD Protections?

If you are being contacted or sued by a debt collector in New York City, here is a practical action plan to make use of the SHIELD Rule and other New York protections:

- Save every letter, email, and text. Keep a file with all collection letters, emails, text messages, and call logs, including dates and times, to document how often collectors are contacting you.

- Write down call details. Note each call: date, time, who called, what was said, any threats, and whether they mentioned lawsuits, wage garnishment, or credit reporting. This helps show if the collector is exceeding contact limits or engaging in harassment.

- Dispute the debt in writing and request verification. Even if time has passed, formally dispute the debt and request documentation that the debt is yours, that the amount is correct, and that it is legally collectible. Under the SHIELD Rule, the collector must pause certain collection efforts and respond within 60 days or risk losing the ability to continue collecting.

- Ask specifically about medical and time‑barred debts. If the debt is medical, ask whether they are reporting it to credit bureaus and remind them that medical debt cannot be furnished under the SHIELD Rule. If the debt is old, ask whether it is time‑barred and whether paying could restart the statute of limitations; collectors must provide prescribed disclosures before collecting on expired debts.

- Do not ignore a summons or complaint. If you receive court papers, you must respond by the deadline to avoid a default judgment, which can lead to wage garnishment and bank restraints. My FAQ on responding to a debt collection lawsuit in New York walks through deadlines, defenses, and what to expect in court:

- Consider demanding substantiation of the debt. New York regulations already allow consumers to demand substantiation of certain charged‑off debts, requiring collectors to provide a package of documents and stop collection efforts until they do. This works alongside the SHIELD Rule’s verification requirements and can be a powerful tool in disputing the debt.

- Get legal advice early. A lawyer experienced in New York City debt collection defense can evaluate whether the collector is complying with SHIELD, the FDCPA, and New York law, and can raise these violations as defenses or counterclaims.

The Law Offices of Robert J. Nahoum, P.C. defends consumers sued by debt collectors, debt buyers, and collection law firms throughout New York, including New York City. If you have been contacted or sued and believe your SHIELD Rule rights may have been violated, you can learn more and request a consultation at https://nahoumlaw.com.

How do I contact The Law Offices of Robert J. Nahoum, P.C.?

If you have been sued by a debt collector, received a default judgment notice, or discovered that your wages or bank account are being hit by a judgment creditor, we can help.

Contact The Law Offices of Robert J. Nahoum, P.C. for a free consultation:

- Phone: (845) 232‑0202

- Website: https://www.nahoumlaw.com

Disclaimer: This FAQ is for general informational purposes only and is not legal advice. Exemption laws change, and how they apply depends on your specific facts. You should consult with an attorney about your situation before taking any action.