By: Robert J. Nahoum

Long-Term Auto Loans Are a Growing Problem

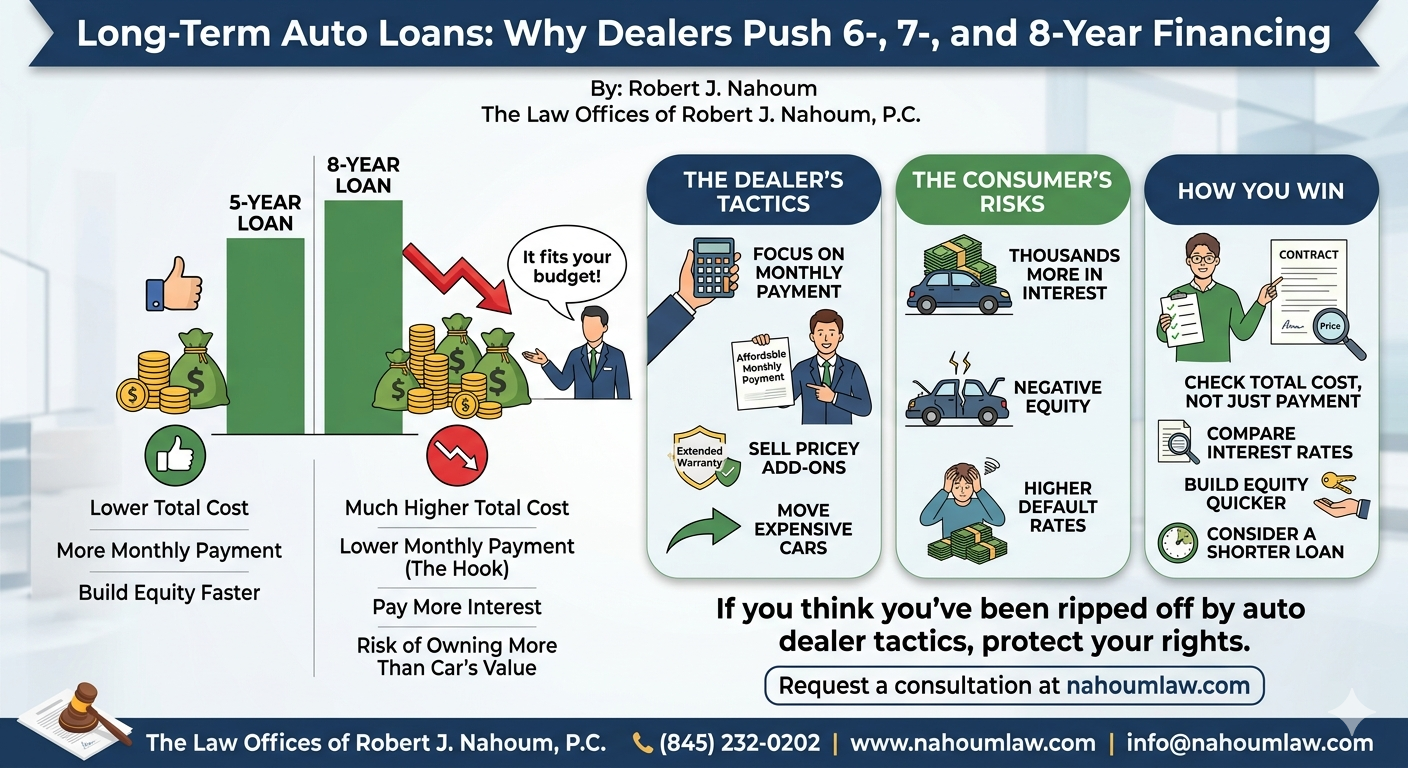

Auto dealers increasingly steer buyers into loans longer than five years because the monthly payment looks more affordable, even though the total cost is much higher. The Consumer Financial Protection Bureau reported that 42 percent of auto loans made in the prior year had terms of six years or more, up from 26 percent in 2009, and that these longer loans are riskier and more expensive for consumers. New York City’s Department of Consumer Affairs has also warned that dealers use longer-than-necessary repayment terms as a common tactic in predatory auto sales.

Why Dealers Like Long Terms

A long loan term is easy to sell because it lowers the monthly payment enough to fit a buyer’s budget on paper. That can help a dealer close a deal, move higher-priced inventory, and sometimes sell add-ons at the same time. But the “affordable payment” pitch often hides the real issue: the buyer is paying far more over the life of the loan.

Why Consumers Lose

Longer loans mean more interest charges, which increases the total amount paid for the car even when the sticker price stays the same. Long-term financing typically carries higher interest and that a higher rate means paying much more over the life of the contract. The CFPB also found that six-year loans are used to finance larger amounts, are associated with lower credit scores, and have higher default rates than shorter loans.

How Much More You Pay

Here is the basic math: if two buyers finance the same car, the buyer with the longer term may have a lower monthly payment, but the lender collects interest for many more months. That is why a car that should cost one amount can end up costing thousands more over time. The CFPB noted that longer-term loans are more likely to result in default, and that some consumers can still owe money even after the vehicle is no longer drivable or has lost substantial value.

Common Dealer Tactics

Dealers may present the long-term loan as the only way to “make the deal work,” especially when the buyer has a trade-in, negative equity, or limited cash for a down payment. They may also bundle the loan with pricey add-ons or use payment-focused sales tactics that keep the buyer from comparing the total amount financed. New York City’s report specifically identified tactics such as deceiving consumers into longer-than-necessary repayment terms and expensive add-on products that are misrepresented as required for financing.

What Buyers Should Watch

Consumers should focus on the total purchase price, the interest rate, and the total of payments, not just the monthly number. A shorter loan term is usually better if the payment can be managed, because it reduces interest and helps the buyer build equity faster. The CFPB’s guidance is clear that consumers should compare costs over the life of the loan, not just the monthly bill.

When It Becomes Auto Fraud

A long-term loan is not automatically unlawful, but it can become part of a fraud or deception case if the dealer misrepresents the financing, hides key terms, or pressures the buyer into a transaction that is materially different from what was promised. If a dealer tells a consumer they are getting a short-term, affordable deal and the paperwork reveals something much worse, that can raise serious consumer-protection issues., The Law Offices of Robert J. Nahoum, PC, represents consumers who have been ripped off by auto dealers and helps them pursue remedies under New York and New Jersey law.

Contact The Law Offices of Robert J. Nahoum, P.C. through nahoumlaw.com for a consultation about your rights and options.

The Law Offices of Robert J. Nahoum, P.C

(845) 232-0202

www.nahoumlaw.com

info@nahoumlaw.com