By: Robert J. Nahoum

When consumers shop for a new or used vehicle, the financing process can often feel overwhelming. Between confusing paperwork, add-on products, and complex interest rates, it is easy for hidden fees or deceptive practices to slip through the cracks. For most individuals, the thought of hiring an attorney to fight an auto finance dispute sounds far too expensive.

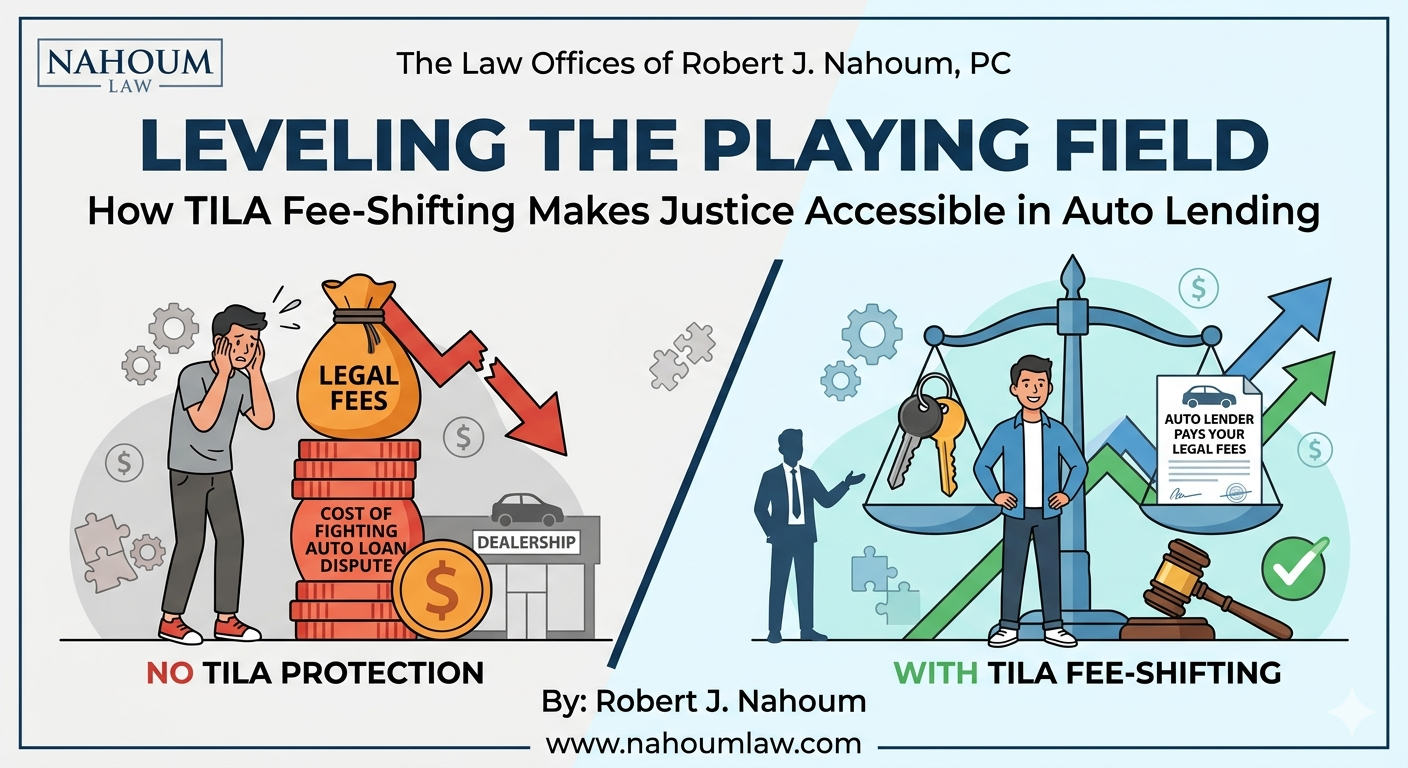

Fortunately, consumer protection laws are designed with built-in mechanisms to level the playing field. Chief among these is the “fee-shifting” provision found in the Truth in Lending Act (TILA).

Understanding how fee-shifting works reveals exactly how everyday consumers can enforce their rights without the burden of paying expensive legal fees.

What is the Truth in Lending Act (TILA)?

The Truth in Lending Act (TILA) is a federal law designed to promote the informed use of consumer credit by requiring clear, uniform, and standardized disclosures of credit terms and costs. In the context of auto lending, TILA mandates that dealerships and finance companies clearly disclose critical terms such as the Annual Percentage Rate (APR), the finance charge, the amount financed, and the total of payments.

When a dealer or lender fails to make these required disclosures accurately, or engages in deceptive lending practices, the consumer may be entitled to hold them accountable.

How Fee-Shifting Works in Consumer Protection Laws

Many of our most effective consumer protection laws, including TILA, contain fee-shifting provisions. But what does that mean?

Normally, when someone hires a lawyer, they pay a flat fee or more commonly, an hourly rate with a substantial upfront retainer. However, in TILA cases, the fee-shifting provision states that if a consumer wins their case, the court requires the violating dealer or lender to pay the consumer’s reasonable attorney’s fees and court costs in addition to the actual damages.

This mechanism serves several vital purposes:

- Removing Financial Barriers

The prospect of spending thousands of dollars in legal fees to correct a lending fraud often discourages consumers from seeking justice. Fee-shifting ensures that financial means do not dictate who gets access to legal representation and who does not.

- Making Claims Economically Viable

The damages in an individual consumer protection dispute might be modest relative to the cost of litigation. Fee-shifting ensures that attorneys can take on important, smaller-scale cases by knowing that their fees are recoverable from the responsible party if the consumer prevails.

- Creating Accountability for Lenders and Dealers

By holding violators responsible for legal costs, fee-shifting provides a powerful incentive for dealerships and auto finance companies to comply strictly with the law.

The Role of Fee-Shifting in Auto Lending Disputes

In the auto sales industry, fee-shifting provisions empower consumers to challenge violations such as:

- Undisclosed or hidden fees: Unlawful additions to the cost of the vehicle that are buried in the financing documents.

- Miscalculated APRs: Deceptive terms that overstate the cost of borrowing.

- Falsified credit terms: Changing the agreed-upon contract terms after the consumer has driven off the lot (often related to “yo-yo” sales tactics).

By utilizing these legal tools, consumers can seek remedies such as statutory damages, actual damages, and the reimbursement of legal fees, all while ensuring that their case is handled professionally.

How Fee-Shifting Enables Contingency Representation

One of the most significant practical benefits of TILA’s fee-shifting provision is that it allows consumer protection attorneys to take cases on a contingency basis.

When a lawyer handles a case on a contingency fee arrangement, the client does not pay out-of-pocket for legal services as the case progresses. Instead, the attorney’s fees are paid either as part of a settlement or when the consumer wins at trial. Because TILA requires the losing defendant to pay the consumer’s attorney’s fees, this framework removes the financial risk for the client.

For the consumer, this means that even if a dispute involves complex auto fraud, deceptive financing, or hidden add-ons, you can secure high-quality legal representation without having to worry about hourly legal bills. If the case is won, the dealer or lender pays the legal fees directly.

Exercising Your Consumer Rights

If you suspect that your auto loan contains undisclosed charges, inflated interest rates, or deceptive practices, you do not have to navigate the complex legal system alone. Thanks to the fee-shifting provisions in laws like TILA, experienced legal representation is within reach.

To learn more about your rights, explore the following resources from our auto fraud lawyer team:

- Learn about your rights under New York consumer laws to fight back against predatory practices.

- Review protections concerning the Electronic Funds Transfer Act if you suspect unauthorized or improper electronic debits.

- Understand the legal boundaries of debt collection on our Fair Debt Collection Practices Act (FDCPA) page.

Disclaimer: This blog post is for informational purposes only and does not constitute legal advice. If you are experiencing an auto lending or consumer protection issue, it is highly recommended to consult with a qualified attorney.