By: Robert J. Nahoum

If a debt collector is calling you, sending letters, or threatening legal action, you have important legal protections. The federal Fair Debt Collection Practices Act (FDCPA) gives you the right to ask a collector to validate the debt. In New York, additional state rules let you request substantiation of the debt at almost any time. Understanding these rights can stop harassment, expose “zombie” debts, and even give you leverage to negotiate or fight the claim.

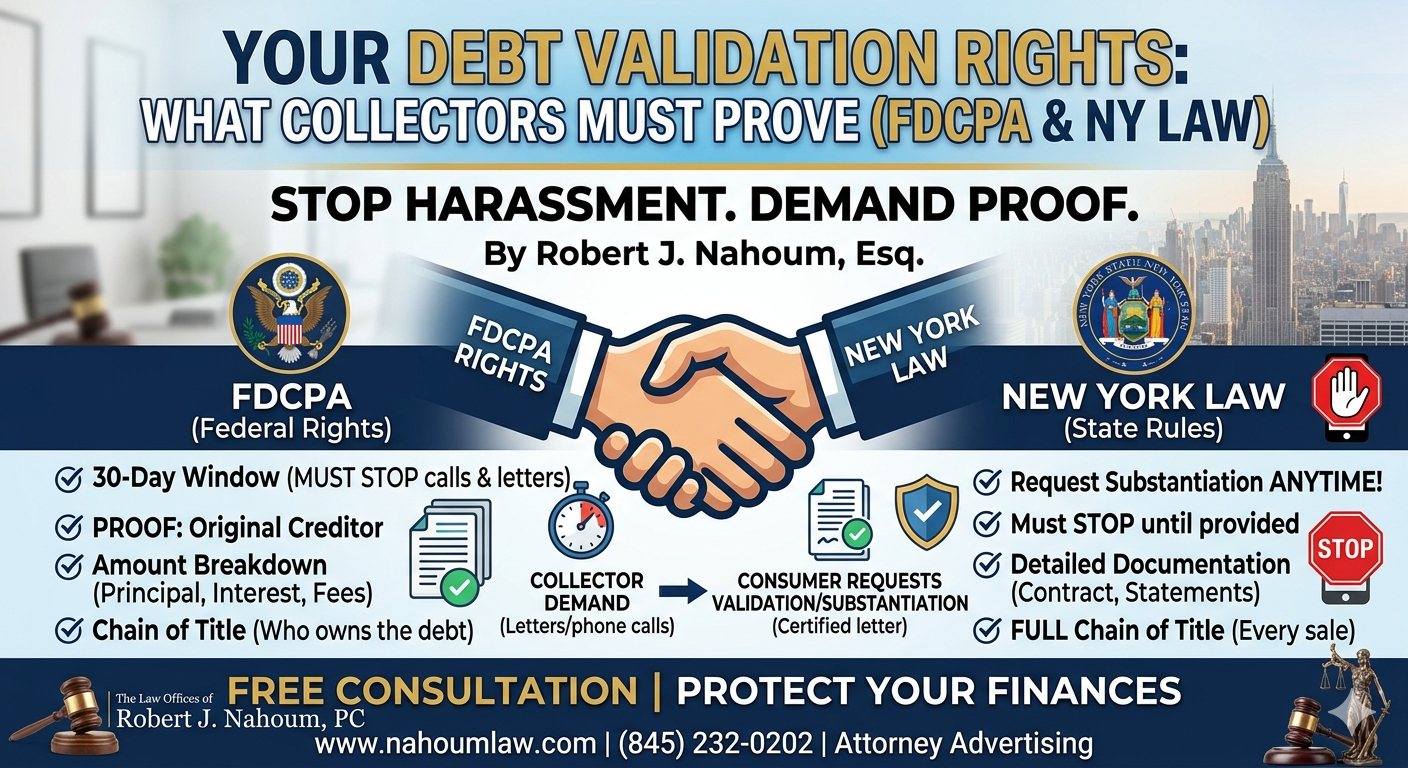

What “Validation Rights” Under the FDCPA Mean

The FDCPA is a federal law that limits how debt collectors can communicate with you and guarantees your right to know what they say you owe. At the core of this protection is the concept of debt validation.

Under 15 U.S.C. § 1692g(a), when a debt collector first contacts you about a debt, they must provide certain “validation information” within five days of that initial contact, if the notice is in writing. This information includes:

- The amount of the debt, broken down into principal, interest, fees, and payments.

- The name of the original creditor.

- A statement that, within 30 days, you can request written verification of the debt or dispute it in writing.

- A notice that, if you dispute the debt during that 30‑day window, the collector must cease collection efforts until they send you verification.

This notice is often called the “validation notice” or “FDCPA validation disclosure.” It can be delivered in writing, by email.

When You Can Request Validation

You are not required to accept a collector’s claim at face value. The FDCPA gives you a 30‑day “dispute window” that starts when you receive the validation notice, not when the collector mailed it.

During this 30‑day period you can:

- Send a written debt validation letter asking the collector to prove the debt is valid.

- Dispute the debt in whole or in part (for example, if you say the amount is wrong or the debt is not yours).

If you make a valid dispute or request for validation within that 30 days, the collector generally must stop all collection activity—no calls, letters, or threats—until they mail you proper verification.

How to Request Validation of a Debt

To protect your rights, validation requests should be in writing and clearly state your intent. Here’s what you should include in a typical validation demand:

- Your full name and address.

- The account number or reference number the collector provided.

- A statement that you are disputing the debt under 15 U.S.C. § 1692g and requesting written verification.

- A request for documentation such as a copy of the original contract, account statements, or proof of the collector’s right to collect the debt.

You should send this letter by certified mail with return receipt requested (or by a similarly trackable method) so you can prove when you sent it. Keep a copy of the letter and all related collection letters, emails, or voicemails; this documentation can be crucial if the collector later violates the FDCPA or brings a lawsuit.

What the Debt Collector Must Do to Comply

Once you request validation within the 30‑day window, the collector must respond in a way that complies with the FDCPA.

In practice, this means:

- The collector must stop contacting you for that debt until it sends you verification.

- The collector must provide sufficient proof that:

- You owe the debt.

- The amount claimed is accurate.

- The collector has the legal right to collect it.

If the collector continues to call or threaten you after receiving your timely validation request, without first sending proper verification, it may be violating the FDCPA. Consumers who experience such violations can seek damages and attorney’s fees under the law.

Requesting Validation After 30 Days

You can still send a dispute or a request for validation after the initial 30-day period has passed, but the rules change significantly:

- No Mandatory Cease: The debt collector is not legally required to stop collecting while they process your request. They can continue to call, write, and even initiate or proceed with a lawsuit.

- Presumption of Validity: Under the FDCPA, if you do not dispute within 30 days, the collector is allowed to assume the debt is valid. This doesn’t mean you legally owe it or can’t challenge it in court later, but it removes the “stop-the-clock” protection afforded by a timely request.

Comparing FDCPA Validation With New York “Substantiation”

New York law adds an extra layer of protection beyond the FDCPA. Under New York Department of Financial Services (DFS) rules and related debt‑collection regulations, consumers can request substantiation of a debt at almost any point in the collection process, not just within the narrow 30‑day window.

Here’s how validation under the FDCPA compares with substantiation under New York law:

| Feature | FDCPA Validation (Federal) | New York Substantiation (State) |

| When you can request it | Within 30 days of receiving validation notice | At any time during the collection process |

| Effect on collection activity | Must stop until validation is provided | Must stop until substantiation is provided |

| Scope of proof required | Basic verification of amount and creditor | Full “chain‑of‑title” and underlying documents (e.g., contracts, statements, charge‑off proof) |

| Applicable to | All consumer debt collectors subject to the FDCPA | Collectors operating in New York who must comply with DFS and state rules |

New York’s substantiation rules require the collector to provide more detailed documentation, such as:

- The original signed contract or account‑opening documents.

- The most recent statement showing transactions (for revolving credit).

- The charge‑off or equivalent statement.

- A clear chain of title showing each sale or assignment of the debt.

Because substantiation can be requested at any time, New York consumers have a powerful tool to interrupt collection efforts, expose errors, and challenge questionable or “zombie” debts—debts that may be too old to legally sue on.

How These Rights Help You in Practice

Knowing your validation and substantiation rights does more than just give you a one‑time pause on collection calls. It can:

- Freeze collection efforts while you investigate the debt.

- Reveal missing or inaccurate records that undermine the collector’s case.

- Help you negotiate a lower settlement or even get the debt removed from your credit report.

- Create grounds for a lawsuit against the collector if it ignores your requests or continues harassment.

If you’re being pursued by a debt collector, you do not have to handle this alone. A consumer‑rights attorney can help you draft and send a proper validation or substantiation letter, respond to any lawsuit, and hold abusive collectors accountable under both federal and New York law.

Get Help With Your Debt Collection Case

If a debt collector is calling you, sending letters, or threatening legal action, you may have strong rights under the FDCPA and New York debt‑collection rules. Understanding your validation and substantiation rights is the first step toward stopping harassment and protecting your finances.

At Nahoum Law, we regularly represent consumers who are being pursued by debt collectors, helping them enforce their rights under the FDCPA and New York law.

If you want to learn more or review a recent collection letter or notice you received, visit our debt collection defense page or contact us to schedule a consultation.

Contact Nahoum Law for FDCPA Help

Facing FDCPA violations from aggressive texts or emails? Nahoum Law specializes in consumer debt defense. Visit our debt collection harassment page or contact us for a free consultation. Read more on FDCPA rights and protect your rights today.

If you need help settling or defending a debt collection lawsuit, stopping harassing debt collectors or suing a debt collector, contact us today to see what we can do for you. With office located in the Bronx, Brooklyn and Rockland County, the Law Offices of Robert J. Nahoum defends consumers in debt collection cases throughout the Tristate area including New Jersey.

The Law Offices of Robert J. Nahoum, P.C

(845) 232-0202

www.nahoumlaw.com

info@nahoumlaw.com

Attorney Advertising Disclaimer: This blog post is for general informational purposes only and does not constitute legal advice. Laws vary by state, and outcomes depend on specific facts. Consult an attorney for personalized guidance. Prior results do not guarantee similar outcomes.