By: Robert J. Nahoum

What the FDCPA means by “debt”

The Fair Debt Collection Practices Act (FDCPA) protects consumers from abusive, deceptive, and unfair collection practices. At the heart of the law is its definition of “debt”:

“Any obligation or alleged obligation of a consumer to pay money arising out of a transaction in which the money, property, insurance, or services which are the subject of the transaction are primarily for personal, family, or household purposes.”

In plain English, this means the FDCPA generally covers consumer debts—the kinds of money you owe from everyday living, not business‑driven obligations.

If the FDCPA does not apply, you may still have protections under other laws (like the Consumer Financial Protection Bureau rules or New York state law), but the powerful “fee‑shifting” leverage of the FDCPA generally won’t be available.

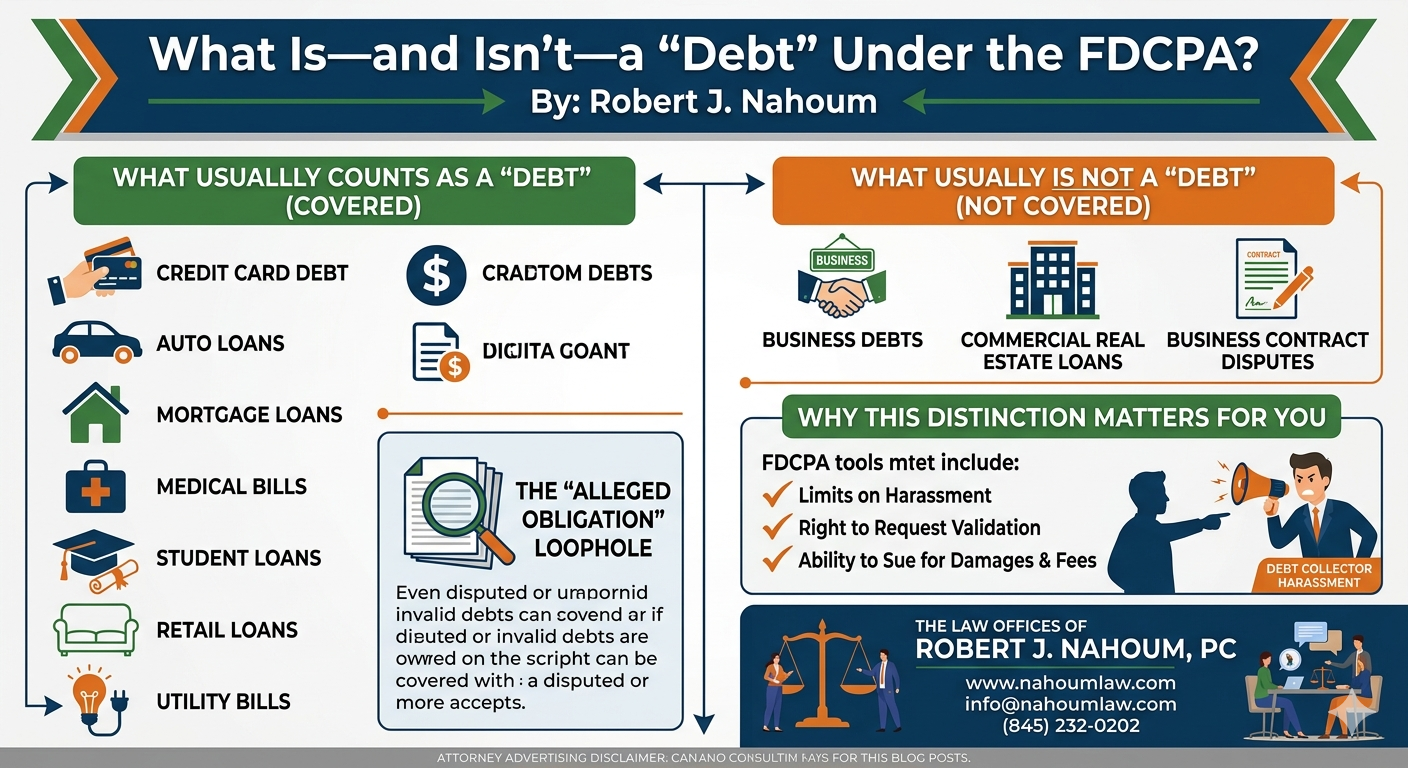

What usually counts as a “debt” under the FDCPA

Courts and regulators interpret the FDCPA definition broadly when the debt is personal, family‑related, or household‑related. Typical examples include:

- Credit card debt (ordinary personal cards, not business‑only lines).

- Auto loans for personal vehicles.

- Mortgage loans on a home you live in.

- Medical bills for yourself or a family member.

- Student loans used for your education.

- Retail or personal loans (e.g., furniture, appliances, personal cash‑advance loans).

- Past‑due utility or telecom bills for your home (electricity, gas, phone, internet).

If a third‑party debt collector is trying to collect one of these consumer obligations, you may be able to sue for harassment, false statements, or other FDCPA violations, and in many cases obtain statutory damages and attorneys’ fees without paying your lawyer out of pocket.

What usually is not a “debt” under the FDCPA

The law is very clear that the FDCPA is not a shield for business‑related or commercial‑type obligations unless they are clearly tied to personal, family, or household use.

Common types of obligations that do not qualify as “debts” under the FDCPA include:

- Business debts (e.g., loans your LLC or corporation took out to fund operations, inventory, or equipment).

- Commercial real estate loans or other business‑purpose loans secured by property used for business.

- Disputes over business contracts or service agreements that are not primarily for personal or family purposes.

If a collector is targeting you only in your business capacity (for example, calling you at work about a company‑name loan), the FDCPA generally will not apply, though you may still have protections under other federal or state laws.

The “alleged obligation” loophole

The FDCPA definition uses the phrase “any obligation or alleged obligation of a consumer to pay money”, which means it can cover even debts that are disputed or might not actually be owed.

If a collector tries to collect an amount that you never incurred, that is already paid, or that is otherwise invalid, the FDCPA can still apply, because the law protects you from how the collector pursues the claimed debt, not whether the debt is ultimately valid.

That is why validation notices, disputes, and cease‑and‑desist letters matter so much: they trigger the collector’s duty to prove what they say they are collecting.

Why this distinction matters for you

If the FDCPA applies, you get strong tools:

- Limits on harassment, threats, and false statements.

- The right to request written validation of the debt.

- The ability to sue for statutory damages, actual damages, and attorneys’ fees if a collector violates the law.

If you are being harassed over a consumer debt (like a credit card, medical bill, or auto loan), you may be able to hold the collector accountable under the FDCPA. For more information, see our page on Debt Collector Harassment, where we explain what kinds of behavior can give rise to a lawsuit.

If you are unsure whether your situation involves a covered “debt,” or if you are being pursued over a business‑type obligation, it is worth speaking with a consumer‑protection attorney who regularly handles FDCPA cases. Our firm, The Law Offices of Robert J. Nahoum, routinely represents consumers harassed by debt collectors and can help you determine whether the FDCPA—and a potential lawsuit—can protect you.

Contact The Law Offices of Robert J. Nahoum, PC today for a consultation.

Facing FDCPA violations from aggressive texts or emails? Nahoum Law specializes in consumer debt defense. Visit our debt collection harassment page or contact us for a free consultation. Read more on FDCPA rights and protect your rights today.

If you need help settling or defending a debt collection lawsuit, stopping harassing debt collectors or suing a debt collector, contact us today to see what we can do for you. With office located in the Bronx, Brooklyn and Rockland County, the Law Offices of Robert J. Nahoum defends consumers in debt collection cases throughout the Tristate area including New Jersey.

The Law Offices of Robert J. Nahoum, P.C

(845) 232-0202

www.nahoumlaw.com

info@nahoumlaw.com

Attorney Advertising Disclaimer: This blog post is for general informational purposes only and does not constitute legal advice. Laws vary by state, and outcomes depend on specific facts. Consult an attorney for personalized guidance. Prior results do not guarantee similar outcomes.