By: Robert J. Nahoum

Are You Being Harassed? Understanding Who the FDCPA Actually Regulates

If you are receiving constant phone calls or threatening letters about an unpaid bill, you have likely heard of the Fair Debt Collection Practices Act (FDCPA). This federal law is a powerful shield that protects consumers from abusive, deceptive, and unfair collection tactics.

However, a common point of confusion for many New Yorkers is realizing that the FDCPA does not apply to everyone who asks you for money. The law specifically targets “debt collectors,” a term defined by the law.

To know if your rights are being violated, you first need to determine if the person calling you fits the legal definition of a debt collector.

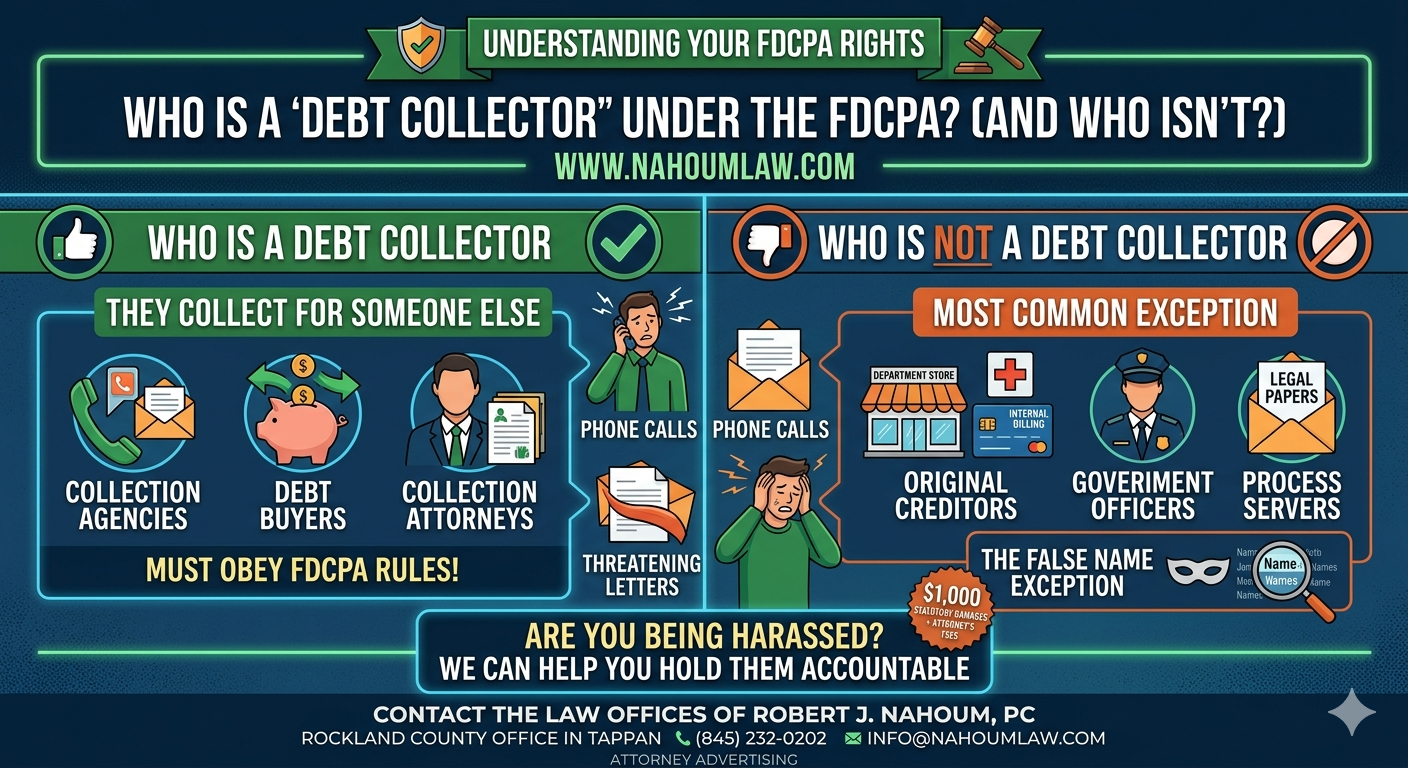

Who IS a Debt Collector?

Under the FDCPA, a debt collector is generally defined as any person or business that uses interstate commerce (like the mail or phones) to collect debts owed to someone else.

Common examples include:

- Third-Party Collection Agencies: Companies hired by a creditor to recover past-due accounts.

- Debt Buyers: Companies that purchase “charged-off” debt for pennies on the dollar and then try to collect the full amount for their own profit.

- Collection Attorneys: Law firms that regularly engage in debt collection litigation or activities.

If you are dealing with any of these entities and they are using high-pressure tactics, you should learn more about your rights under the FDCPA.

Who IS NOT a Debt Collector?

The FDCPA typically does not apply to “original creditors.” This is the most significant exception to the rule.

- Original Creditors: If you owe money to a department store, a local hospital, or a bank where you opened a credit card, and their own internal billing department calls you, they are generally not considered “debt collectors” under the federal FDCPA.

- Government Officers: Individuals performing their official duties (such as a court official serving a notice).

- Process Servers: People whose only role is to deliver legal papers for a lawsuit.

The “False Name” Exception

There is one major trap for creditors: If an original creditor uses a different name that implies a third party is collecting the debt (making it look like they hired a collection agency when they didn’t), they can suddenly be treated as a “debt collector” and must follow all FDCPA rules.

Why the Distinction Matters

If a person or company meets the FDCPA definition of a debt collector, they are prohibited from, among other things:

- Calling you before 8:00 AM or after 9:00 PM.

- Using profane or abusive language.

- Threatening legal action they do not intend to take.

- Contacting your friends, family, or employer about your debt.

When a debt collector breaks these rules, they may be liable to you for statutory damages up to $1,000, actual damages, and your attorney’s fees.

Take Action Against Harassment

Identifying the player is the first step in winning the game. If you are being pursued for a debt, it is vital to document every call and keep every letter.

If you suspect a debt collector has crossed the line, we can help you hold them accountable. Visit our practice area page on debt collection harassment to see how we protect consumers from unfair practices.

Contact The Law Offices of Robert J. Nahoum, PC today for a consultation.

Facing FDCPA violations from aggressive texts or emails? Nahoum Law specializes in consumer debt defense. Visit our debt collection harassment page or contact us for a free consultation. Read more on FDCPA rights and protect your rights today.

If you need help settling or defending a debt collection lawsuit, stopping harassing debt collectors or suing a debt collector, contact us today to see what we can do for you. With office located in the Bronx, Brooklyn and Rockland County, the Law Offices of Robert J. Nahoum defends consumers in debt collection cases throughout the Tristate area including New Jersey.

The Law Offices of Robert J. Nahoum, P.C

(845) 232-0202

www.nahoumlaw.com

info@nahoumlaw.com

Attorney Advertising Disclaimer: This blog post is for general informational purposes only and does not constitute legal advice. Laws vary by state, and outcomes depend on specific facts. Consult an attorney for personalized guidance. Prior results do not guarantee similar outcomes.