By: Robert J. Nahoum

When you walk into a dealership to buy a car, the excitement of driving off the lot can sometimes overshadow the fine print of the financing paperwork. For most of us, an auto loan is one of the largest financial commitments we make. But did you know there is a powerful federal law designed to ensure you know exactly what you are paying for?

It’s called the Truth in Lending Act (TILA), and it plays a vital role in keeping auto lending honest, transparent, and fair.

What is the Truth in Lending Act (TILA)?

Enacted in 1968, TILA is a federal law designed to promote the informed use of consumer credit. By requiring uniform, meaningful disclosure of costs and terms, TILA ensures that consumers can compare credit terms more readily and avoid the uninformed use of credit.

While TILA is perhaps most famous for its role in mortgages and credit cards, it applies directly to auto financing when credit is offered by a dealer or lender who regularly extends credit and the loan involves a finance charge or is payable in more than four installments.

Key TILA Protections in Auto Financing

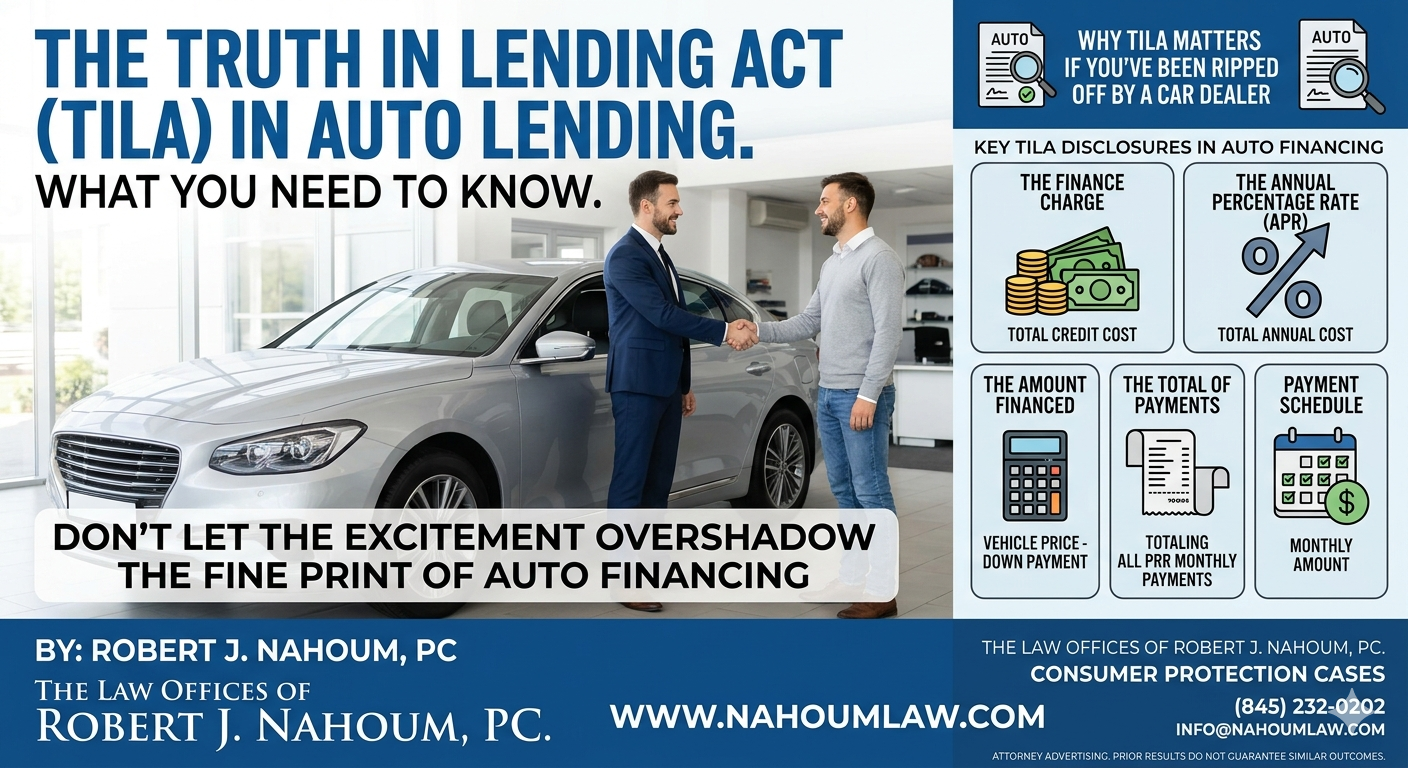

When you finance a vehicle, TILA requires dealerships and lenders to disclose specific information clearly and conspicuously before the transaction is finalized. Here is what you must be provided:

- The Finance Charge

TILA mandates that the exact cost of the credit must be disclosed as a dollar amount. This includes not just the interest rate, but also fees for processing, document preparation, and other required credit-related charges.

- The Annual Percentage Rate (APR)

The APR represents the total cost of credit on a yearly basis, expressed as a percentage. It allows consumers to compare loans from different institutions consistently. Without this standardized figure, a dealership could manipulate interest and fees, making it incredibly difficult to compare costs.

- The Amount Financed

This is the actual amount of credit provided to you. It is calculated by taking the cash price of the vehicle, subtracting any down payment or trade-in value, and adding other amounts financed (such as credit insurance or extended warranties) that are paid for out of the loan.

- The Total of Payments

This figure tells you the total amount you will have paid after you have made all scheduled payments over the life of the loan. It shows the true cumulative cost of purchasing the vehicle with credit.

- Payment Schedule

TILA requires a clear breakdown of when your payments are due, the total number of payments, and the dollar amount of each individual payment.

Why TILA Matters If You’ve Been Ripped Off by a Car Dealer

In the auto sales industry, hidden fees, inflated interest rates, and unauthorized add-on products are unfortunately common. Dealerships that violate TILA by failing to disclose these terms accurately leave themselves open to legal action.

If you suspect that your auto loan paperwork does not match the terms you agreed to, or if the disclosures were hidden, misleading, or omitted entirely, you may have legal recourse. For more information on how to protect yourself or to read about past cases, feel free to review our case results or learn more about our firm and the types of consumer protection cases we handle.

Taking Action Against Auto Fraud

Understanding your rights under the Truth in Lending Act is only the first step. If a car dealership has engaged in deceptive practices, consumer protection laws are on your side.

If you feel you have been taken advantage of or that your rights have been violated during an auto purchase, please contact us today to discuss your situation and see how we can help.

Contact The Law Offices of Robert J. Nahoum, P.C. through nahoumlaw.com for a consultation about your rights and options.

The Law Offices of Robert J. Nahoum, P.C

(845) 232-0202

www.nahoumlaw.com

info@nahoumlaw.com

Attorney Advertising Disclaimer: This blog post is for general informational purposes only and does not constitute legal advice. Laws vary by state, and outcomes depend on specific facts. Consult an attorney for personalized guidance. Prior results do not guarantee similar outcomes.