By: Robert J. Nahoum

Auto dealers rarely hand you just one document when you buy a car, and that’s not by accident. Buried in the paperwork are often inconsistencies, hidden fees, or outright misrepresentations. Understanding the difference between the purchase order, bill of sale, and retail installment sales contract can make the difference between a fair deal and getting ripped off.

At Nahoum Law, we regularly review these documents to uncover fraud and hold dishonest auto dealers accountable. Here’s what you need to know.

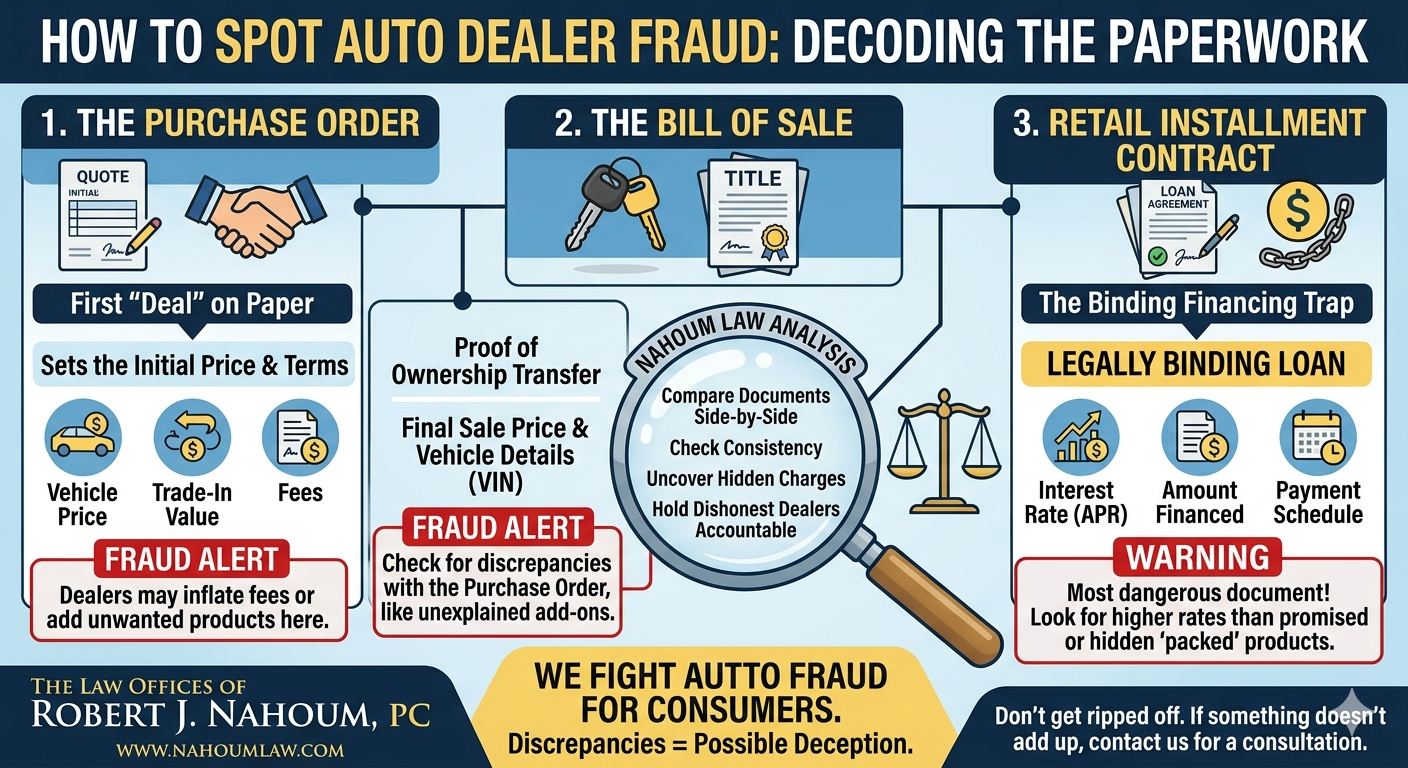

The Purchase Order: The First “Deal” on Paper

The purchase order (sometimes called a buyer’s order) is usually the first document you sign. It lays out the basic terms of the deal:

- Vehicle price

- Trade-in value

- Taxes and fees

- Add-ons (warranties, service plans, etc.)

This document often looks straightforward, but it’s where many deceptive practices begin. Dealers may:

- Inflate fees or add unwanted products

- Misstate the agreed price

- Include vague or conditional language

Importantly, the purchase order is not always the final contract. Dealers sometimes change terms later, hoping you won’t notice.

The Bill of Sale: Proof of Transfer

The bill of sale reflects the actual transfer of ownership. It typically includes:

- Buyer and seller information

- Vehicle details (VIN, make, model)

- Final sale price

In theory, this document should match what you agreed to in the purchase order. In reality, discrepancies are common.

For example, a consumer might agree to pay $25,000, but the bill of sale shows $27,500 due to unexplained add-ons. That gap is often where fraud lives.

The Retail Installment Sales Contract (RISC): The Financing Trap

If you’re financing the vehicle, the retail installment sales contract (RISC) is the most important, and most dangerous, document.

This is the legally binding loan agreement. It includes:

- Interest rate (APR)

- Total amount financed

- Payment schedule

- Finance charges

Dealers sometimes use the RISC to quietly alter the deal. Common issues include:

- Higher interest rates than promised

- Packed products like warranties, service contract, and tire and wheel protection rolled into the loan

Once signed, this document often governs your legal obligations, regardless of what earlier documents said.

How Consumer Protection Lawyers Spot Fraud

When a client comes to us, we don’t look at these documents in isolation, we compare them side by side.

Here’s what we analyze:

- Consistency across documents: Do the numbers match from purchase order to bill of sale to RISC?

- Undisclosed charges: Were fees or products added without clear consent?

- Misrepresentations: Did the dealer promise one thing verbally but document another?

- Illegal practices: Are there violations of New York or Federal consumer protection laws?

Even small discrepancies can signal larger issues. For example, a $1,000 “processing fee” appearing only in the RISC, not the purchase order, can indicate deceptive conduct.

Why This Matters

Auto fraud cases often come down to paperwork. Dealers rely on complexity and volume to overwhelm consumers. But the law doesn’t allow them to hide behind fine print.

If something doesn’t add up in your documents, there’s a good chance it isn’t legal.

At Nahoum Law, we help consumers fight back against deceptive auto dealers and recover damages when fraud occurs.

Protect Your Consumer Rights Today

You don’t have to face predatory auto dealers alone. If you have questions about a recent purchase or believe you were misled by deceptive car advertising in New York, contact us today for a consultation.

Disclaimer: This blog post is for informational purposes only and does not constitute legal advice. If you are experiencing an auto lending or consumer protection issue, it is highly recommended to consult with a qualified attorney.