By: Robert J. Nahoum

Overview of New York vehicle repossession law

In New York, most car loans are “secured transactions,” meaning the lender has a lien on the vehicle and can repossess after a default (usually missed payments) without going to court, as long as it does not “breach the peace.” After repossession, the lender must follow Article 9 of the Uniform Commercial Code (UCC) and New York-specific rules on notices and “commercially reasonable” sale of the car.

If the lender or debt buyer later sues you for a deficiency balance, it has the burden to prove the debt, the amount claimed, and that it complied with repossession and notice requirements.

Required notices and timeframes in New York

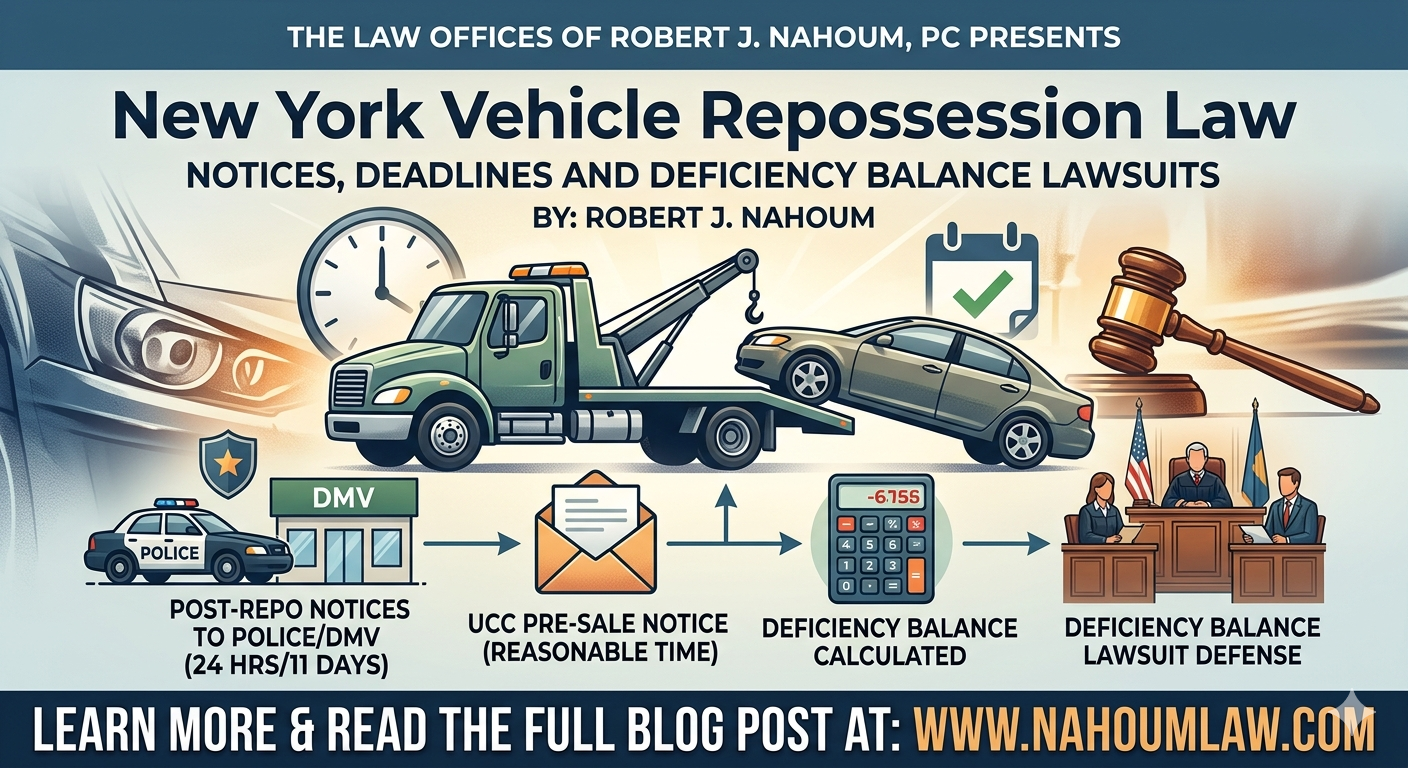

New York law layers together UCC Article 9 and the Vehicle and Traffic Law to create multiple notice requirements around a car repossession.

Key notices and timing:

- Post‑repossession notice to police and DMV: Under New York Vehicle and Traffic Law § 425(1), when a motor vehicle or motorcycle is repossessed, the creditor (or its agent) must notify law enforcement and the vehicle owner within 24 hours, and notify the motor vehicle office within 11 days.

- Notice before disposition (sale) of the vehicle – UCC 9‑611: A secured creditor that plans to sell or otherwise dispose of a repossessed vehicle must send “reasonable” authenticated notification of the disposition to the debtor and any secondary obligor, unless a limited exception applies.

- Content of consumer notice – UCC 9‑614: In a consumer‑goods transaction (which includes most personal car loans), the notice must include, among other items, a description of the collateral, the method of intended disposition, the date, time or earliest time the sale will occur, how the debtor can redeem or reinstate, and a description of potential liability for a deficiency.

- “Reasonable time” before sale: The UCC requires that the pre‑sale notice be sent within a reasonable time before the earliest sale date; while “reasonable” is not hard‑coded to a specific number of days, creditors that rush the process or give only minimal time risk a court finding the notice unreasonable.

- Notice of sale and accounting of proceeds: After the vehicle is sold, the creditor must apply the proceeds to reasonable expenses (including the cost of repossession) and the outstanding balance, and it must be prepared to account for the sale price and how the proceeds were applied if it later claims a deficiency.

If you want more background on secured debts and how repossession fits into the bigger picture of consumer collections, you can read my article “What is a Deficiency Balance?”

What is a “deficiency balance” after repossession?

A “deficiency balance” is the amount left over on the loan after the creditor repossesses and sells the car and applies the sale proceeds to the debt. For example, if you owed $15,000, had paid $1,000, and the lender repossessed and sold the car for $10,000, there could still be a several‑thousand‑dollar deficiency after adding fees and interest.

Under New York Personal Property Law § 315 and UCC § 9‑610, the buyer remains liable for any deficiency after default and repossession, but the deficiency must be calculated in accordance with Article 9 and reduced by a credit similar to the unearned finance charge refund the buyer would have received upon prepayment. Critically, if the creditor failed to give proper notices or to conduct a “commercially reasonable” sale, courts can limit or deny the creditor’s ability to collect a deficiency.

What is a deficiency balance lawsuit?

A deficiency balance lawsuit is a debt collection case where the lender or a debt buyer sues you for the remaining balance after your repossessed vehicle has been sold. The plaintiff might be the original creditor or, very often, a debt buyer that purchased a portfolio of deficiency accounts for pennies on the dollar.

In New York, to win a deficiency balance lawsuit the plaintiff generally must prove:

- That a valid car loan or retail installment contract existed and you are the borrower.

- That you defaulted and the vehicle was lawfully repossessed.

- That all required notices (including the pre‑sale UCC notice) were sent in a timely and compliant manner.

- That the sale of the vehicle was “commercially reasonable,” including the sale price and related expenses.

- That the deficiency amount was correctly calculated under New York law, including any required credits under Personal Property Law § 315.

Debt buyers, in particular, sometimes struggle to produce the complete chain of assignment, the original contract, and the detailed repossession and sale records needed to meet this burden. Challenging the notices, timelines and sale reasonableness can be a powerful defense strategy in New York City consumer courts.

How The Law Offices of Robert J. Nahoum, PC can help

If you are in New York and have been sued for a repossession‑related deficiency balance, or you think your car was repossessed or sold without proper notice, we can review your case and the creditor’s paperwork to identify defenses and potential counterclaims. Our practice regularly defends consumers in debt collection lawsuits and pursues claims against debt collectors who violate federal and New York law.

You can learn more about defending debt collection lawsuits, deficiency balances and other consumer issues on our website at https://www.nahoumlaw.com. If you have been served with a summons, do not ignore it—contact The Law Offices of Robert J. Nahoum, PC to discuss your options and deadlines.

How do I contact The Law Offices of Robert J. Nahoum, P.C.?

If you have been sued by a debt collector, received a default judgment notice, or discovered that your wages or bank account are being hit by a judgment creditor, we can help.

Contact The Law Offices of Robert J. Nahoum, P.C. for a free consultation:

- Phone: (845) 232‑0202

- Website: https://www.nahoumlaw.com

Disclaimer: This FAQ is for general informational purposes only and is not legal advice. Exemption laws change, and how they apply depends on your specific facts. You should consult with an attorney about your situation before taking any action.