By: Robert J. Nahoum

What Is a Wage Garnishment (Income Execution) in New York?

In New York, wage garnishment is called an income execution and is governed primarily by CPLR §5231. An income execution is a court-backed order directing that a portion of a judgment debtor’s paycheck be withheld and paid toward a debt collection judgment.

Before a creditor can garnish wages, it must first sue, win the case, and obtain a money judgment against the consumer. Once the creditor becomes a judgment creditor, its debt collection lawyers can use tools like information subpoenas, bank levies, and income executions to turn that paper judgment into money.

How Judgment Creditor Debt Collection Lawyers Start a Wage Garnishment

Once a judgment is entered, a judgment creditor’s attorney can start the income execution process by preparing and issuing an income execution to the sheriff (or a NYC marshal). The income execution states the amount of the judgment, interest, and costs, and it identifies the judgment debtor and the employer if known.

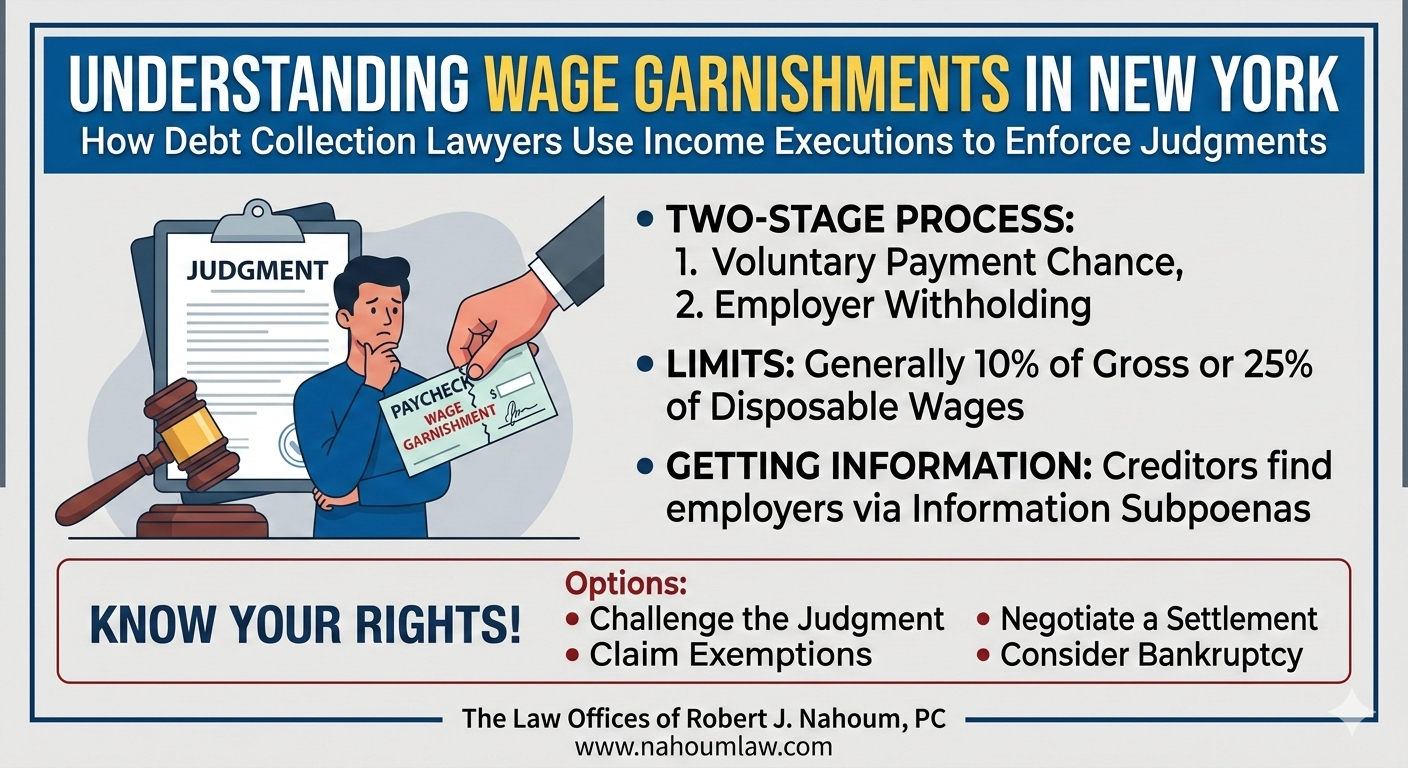

New York uses a two‑stage process:

- Stage One – Direct to the Debtor:

- The sheriff or marshal first serves the income execution on the judgment debtor, usually by mail, giving the debtor a chance to make voluntary payments directly.

- The execution typically directs the debtor to begin sending installments (up to 10% of gross income) to the sheriff immediately, within New York’s statutory limits.

- Stage Two – Employer Wage Withholding:

- If the debtor does not comply with the voluntary installment plan, the sheriff or marshal can then serve the income execution on the employer.

- Once served, the employer must withhold the specified percentage from each paycheck and remit it to the sheriff, who then forwards funds to the judgment creditor.

If the employer fails to honor the income execution, the judgment creditor can bring a proceeding against the employer for the missed installments.

How Much of Your Paycheck Can Be Garnished?

Wage garnishment amounts in New York are limited by both federal and state law. In general, New York allows the lesser of:

- 10% of your gross wages, or

- 25% of your disposable (after‑tax) earnings,

- and only from the portion of earnings that exceeds 30 times the greater of the state or federal minimum wage.

New York is more protective than many states; if you earn below a certain weekly amount after taxes (around the level of 30 times the applicable minimum wage), your wages may not be garnished at all. On top of that, only one judgment creditor can garnish wages at a time in most consumer cases, which can limit how much is taken from each check.

Support obligations such as child support and spousal support follow different, higher federal limits and are enforced through separate mechanisms under CPLR §5241, not standard consumer debt income executions.

For a practical FAQ on how much can be taken and what to do when you receive a notice, see my guide “How to Respond to a Wage Garnishment Notice in New York” at https://nahoumlaw.com/how-to-respond-to-a-wage-garnishment-notice-in-new-york-faq-guide/.

How Wage Garnishment Fits Into Debt Collection Judgment Enforcement

Income executions are one of several powerful post‑judgment remedies available to creditors. After learning where you work—often through an information subpoena or prior credit application—the judgment creditor’s attorney will choose wage garnishment when:

- You are steadily employed and receive regular wages or salary.

- There are few reachable bank accounts or non‑exempt assets to levy.

- The creditor wants a predictable stream of payments over time rather than a single lump‑sum levy.

A typical enforcement strategy might look like this:

- Serve an information subpoena to uncover where you work and bank.

- If an employer is identified, issue an income execution to the sheriff to start wage garnishment.

- If bank accounts are identified, use restraining notices and bank levies to seize non‑exempt funds.

Because an income execution can continue until the judgment, interest, and costs are paid (or the judgment expires or is vacated), wage garnishments can last years if left unchallenged.

Your Rights and Options When Facing a New York Income Execution

If you receive a notice of income execution or wage garnishment, you still have important rights and options. Common strategies include:

- Challenging the judgment itself: If you were never properly served with the lawsuit or have a valid defense, you may be able to move to vacate the judgment and stop the garnishment.

- Claiming exemptions and hardship: New York law protects certain minimum income levels and may offer hardship relief where garnishment would prevent you from meeting basic needs.

- Negotiating a settlement or payment plan: In many cases, a negotiated lump‑sum settlement or restructuring of payments can resolve a judgment faster and on better terms.

- Bankruptcy as a last resort: A consumer bankruptcy filing can stop wage garnishments and may discharge the underlying debt in appropriate cases.

The Law Offices of Robert J. Nahoum, P.C. represents New York consumers who are sued by debt collectors and who are facing judgment enforcement, including wage garnishments and bank restraints. You can learn more about our consumer protection and judgment enforcement practice and request a free consultation at https://www.nahoumlaw.com.

If you are already dealing with a wage garnishment or have been threatened with an income execution, visit our page on stopping wage garnishments at https://nahoumlaw.com/stop-garnishments/ or contact us at (845) 232‑0202 to discuss your options.

Disclaimer: This blog post is for informational purposes only and does not constitute legal advice. Every case is different; you should speak with an attorney about your specific situation before making legal decisions.