By: Robert J. Nahoum

What Is “Substantiation” of Debt in New York?

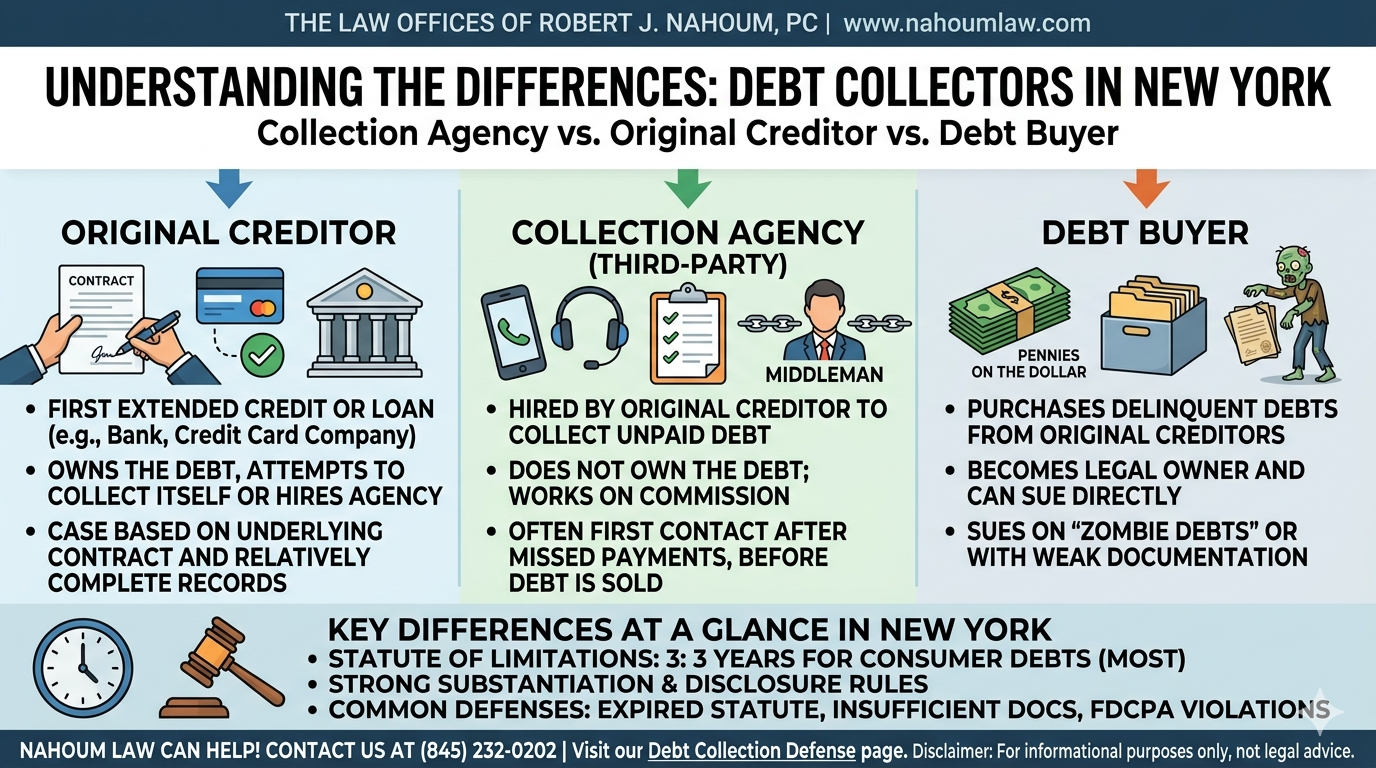

If you live in New York and have been sued or threatened with a lawsuit over a consumer debt, you’ve probably seen one of three names on the summons: an original creditor, a collection agency, or a debt buyer. Knowing who you’re dealing with can make a big difference in how you defend the case and what legal arguments you can raise. This guide explains what each of these terms means and how they operate under New York law.

Who is the original creditor?

An original creditor is the bank, credit‑card issuer, lender, or service provider that first extended credit or gave you a loan. Examples include major credit‑card companies, banks that issued personal loans, or retailers that provided store‑based financing.

- You originally signed a contract directly with the original creditor.

- The creditor may try to collect the debt itself (through an in‑house collections department) or may hire a third‑party collection agency.

If you’re sued by an original creditor, the case is often based on the underlying contract and the creditor’s own records. That means the creditor usually has relatively complete documentation, but it also gives you opportunities to challenge the amount, the statute of limitations, or the chain of documentation.

What is a collection agency?

A collection agency (also called a third‑party collector) is a company that is hired by an original creditor to collect unpaid debts. The agency does not own the debt; it acts as a “middleman” for the creditor.

Key traits of a collection agency:

- Works on commission or a contingency fee, typically a percentage of what it recovers.

- Must disclose that it is collecting for someone else and provide certain required notices under the FDCPA and New York law.

- Often contacts you first after a few months of missed payments, before the debt is sold.

In New York, collection agencies must follow strict rules about harassment, false statements, and improper lawsuits. If you are sued by a collection agency, you can challenge whether the agency has proper authority to sue, whether the debt is valid, and whether the agency has sufficiently substantiated the debt under New York regulations.

What is a debt buyer?

A debt buyer is a company that purchases delinquent debts from original creditors (or sometimes from other collectors) for a fraction of the face value. Once the debt buyer buys the account, it becomes the legal owner of the debt and can sue you directly.

Key points about debt buyers:

- The buyer may pay as little pennies on the dollar of the face value of the debt, based on how likely it believes the account is to be collected.

- Because the documentation is sometimes incomplete or bundled in large portfolios, debt buyers can sometimes struggle to prove the exact amount owed or the chain of ownership.

- Some debt buyers aggressively sue consumers, sometimes over “zombie debts”, debts that are beyond the statute of limitations or already paid.

In New York, debt buyers must still comply with the FDCPA, and special substantiation rules (such as 23 NYCRR § 1.4 on substantiation of consumer debts). If a consumer disputes the debt, the collector must provide detailed evidence that the debt is valid and that the buyer has the right to collect it.

If you are sued by a debt buyer, common defenses include:

- Statute of limitations has expired.

- Insufficient documentation to prove the debt or the transfer of ownership.

- Violations of the FDCPA or New York’s substantiation rules.

Key differences at a glance

| Role | Who owns the debt? | How they get paid | Common legal issues in NY |

| Original creditor | Themselves (original lender) | Through payments or settlements | Contract claims, statute of limitations, proof of account terms |

| Collection agency | The creditor (not the agency) | Commission or percentage of collected amount | FDCPA violations, improper lawsuits, inadequate substantiation |

| Debt buyer | Themselves (purchased the debt) | Profit from recovered amounts they bought cheaply | Zombie debts, weak documentation, substantiation failures |

Why these distinctions matter in New York

In New York, the statute of limitations for most consumer debts (like credit cards, personal loans, and medical bills) is three years from the date of your last payment or written acknowledgment of the debt. If a collection agency or debt buyer tries to sue you after that period, the case may be time‑barred, which can be a powerful defense if you respond to the lawsuit.

New York also has strong substantiation and disclosure rules, requiring collectors to provide clear information about the debt, the original creditor, and your right to dispute the claim. If the collector fails to meet these requirements, you may be able to stop collection activity or even bring a counterclaim.

How Nahoum Law can help you

If you’ve been sued or threatened with a lawsuit by an original creditor, a collection agency, or a debt buyer in New York, it’s important to respond instead of ignoring the case. An experienced consumer‑debt‑defense attorney can review the complaint, challenge the sufficiency of the documentation, and raise affirmative defenses such as the statute of limitations or FDCPA violations.

At The Law Offices of Robert J. Nahoum, PC, we regularly defend New York consumers in debt‑collection lawsuits and help them understand their rights and options. To learn more about how we can assist you, visit our Debt Collection Defense page or contact our office to schedule a consultation.

If you have been contacted by a debt collector contact us at (845) 232‑0202 to discuss your options.

Disclaimer: This blog post is for informational purposes only and does not constitute legal advice. Every case is different; you should speak with an attorney about your specific situation before making legal decisions.