By: Robert J. Nahoum

The Salesperson Isn’t the Real Problem

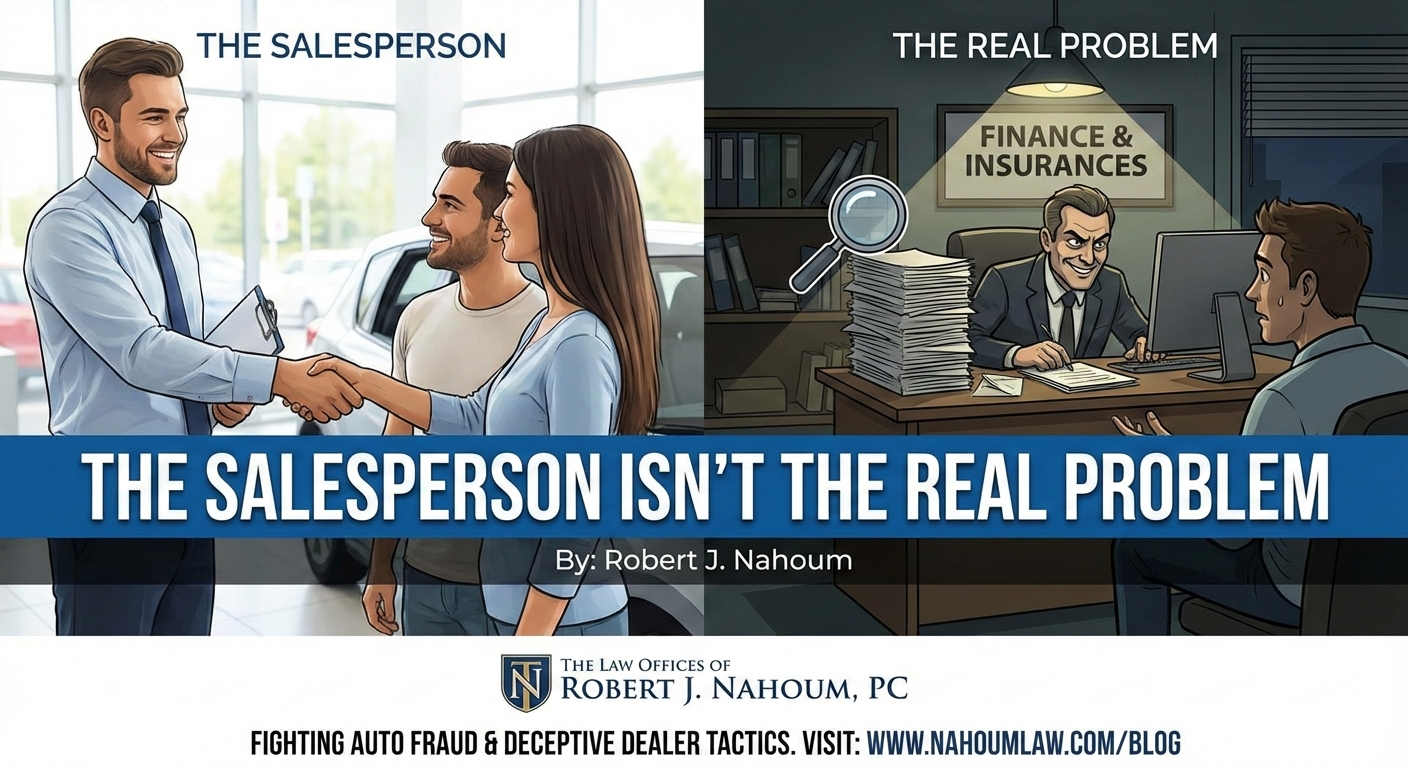

When you walk into a dealership, the first person you meet is usually a smiling salesperson eager to get you behind the wheel. Sure, they might push for a quick sale or talk up a “great deal,” but the real trouble usually starts after you’ve agreed on a price.

That’s when you’re sent down the hall to the Finance and Insurance (F&I) office — the place where the paperwork, and often the dishonesty, really begin.

What Really Happens in the F&I Office

Once you’re in that little office, you’re dealing with the F&I representative. Their title sounds helpful, but remember — this person works for the dealership, not for you. Their job is to finish the paperwork, set up your loan, and sell a bunch of extras that boost the dealer’s profit, like:

- Extended warranties

- GAP insurance

- Tire and wheel protection

- Paint sealant or rustproofing

- Key fob replacement coverage

Nothing wrong with offering products — unless they’re added without your knowledge or the terms are misrepresented to you. Unfortunately, that happens all the time.

Some F&I reps quietly hike up your interest rate, slip extras into the deal, or change figures after you’ve signed. By the time you drive off the lot, your “great deal” could easily cost thousands more than you realized.

How These Tricks Violate the Truth in Lending Act

The Truth in Lending Act (TILA) is a federal law that requires total honesty and transparency in credit deals. It says the lender — and that includes car dealers who arrange financing — must clearly disclose key details like:

- The annual percentage rate (APR)

- The finance charge

- The total amount financed

- The total of all payments

If an F&I rep hides costs, changes the APR, or adds products without disclosure, that’s a violation of TILA. Some of the most common scams include:

- Payment packing: Inflating the monthly payment to sneak in extras you didn’t agree to.

- Interest rate markups: Charging you a higher rate than the bank approved and pocketing the difference.

- Document tampering: Changing or forging paperwork after you’ve signed it.

Each of these not only cheats consumers but also breaks the law.

How to Protect Yourself

A few smart steps can save you a huge headache later:

- Get a loan pre-approval from your bank or credit union before you go car shopping.

- Review every page of the contract — especially the Retail Installment Sales Contract — before you sign anything.

- Say no to products you don’t want or don’t understand.

- Always take copies of everything you sign.

If something doesn’t look right, trust your gut — then talk to a lawyer who knows this stuff inside and out.

We Help Consumers Stand Up to Dishonest Dealers

At The Law Offices of Robert J. Nahoum, P.C., we’ve seen every car dealer trick in the book. We help New York consumers who’ve been scammed fight back under the Truth in Lending Act and state consumer protection laws.

If your loan paperwork doesn’t match what you were promised — or you suspect something shady happened in the finance office — we can help you hold the dealer accountable.

Learn more about auto fraud and consumer protection on our website or reach out for a consultation. When the dealership plays dirty, we help level the playing field.

Contact Us Today

If you believe you’ve been misled, overcharged, or tricked during a car purchase or auto loan, contact The Law Offices of Robert J. Nahoum, P.C. today for a free, confidential consultation. Our team is ready to review your case, explain your rights, and help you recover what’s fair.

For a free consultation about an auto‑fraud or deceptive‑sales issue, contact us at our Hudson Valley office or our Brooklyn location.

📞 Call (845) 232‑0202 or visit our contact page: www.nahoumlaw.com/contact