By: Robert J. Nahoum

What Is “Substantiation” of Debt in New York?

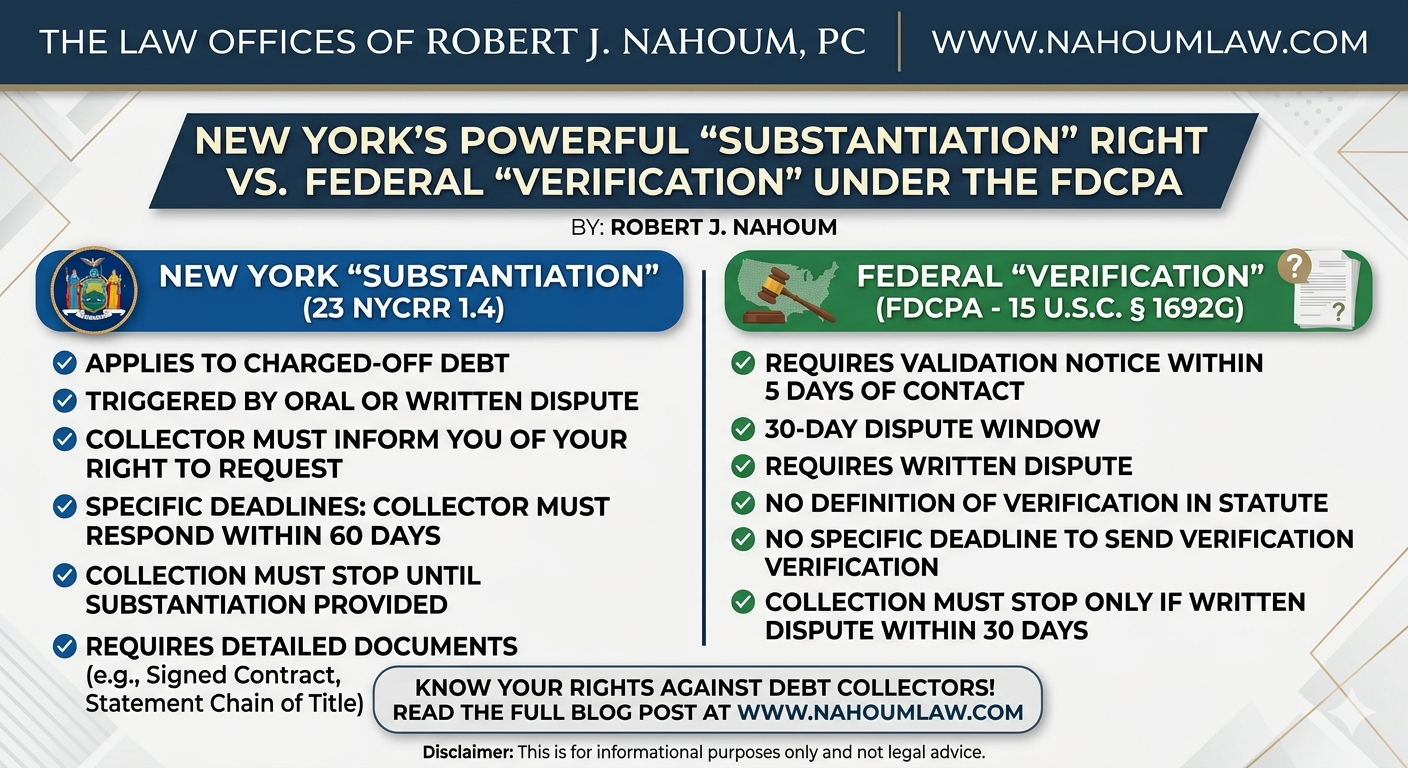

New York has its own debt collection regulations that give consumers a powerful right to demand “substantiation” of a charged‑off debt, a much more robust standard than federal “verification” under the FDCPA. These rules apply to third‑party debt collectors including debt buyers collecting on charged‑off consumer debt in New York State.

Under 23 NYCRR 1.4, if you dispute a charged‑off debt (either orally or in writing), the debt collector must tell you that you can request substantiation of the debt and must provide clear written instructions on how to do it. This requirement exists on top of your federal rights under the Fair Debt Collection Practices Act (FDCPA).

How to Request Substantiation, And Key Deadlines

New York law builds a clear request-and-response process with specific timeframes.

- If you dispute the debt orally, the collector must:

- Explain during that conversation how to make a written substantiation request, and

- Within 14 days, send you written instructions on how to request substantiation.

- If you dispute the debt in writing, the collector has 21 days from receipt of your letter to send you written instructions on how to request substantiation.

- Once you request substantiation, the collector must:

- Provide written substantiation within 60 days, and

- Stop all collection efforts until that substantiation is sent.

If the collector cannot substantiate within 60 days, it still cannot resume collection until it eventually does, and failing to meet the 60‑day deadline is a separate regulatory violation enforceable by the New York Department of Financial Services. In some cases, collectors may choose to extinguish or satisfy the debt instead of providing substantiation.

For more on defending New Yorkers from abusive debt collection, see my FDCPA overview

What Counts as “Substantiation” Under 23 NYCRR 1.4?

New York does not let collectors satisfy their obligations with vague or minimal information. Substantiation must include specific documentation showing that the right consumer is being pursued for the right amount by the right party.

Under 23 NYCRR 1.4(c), substantiation of a charged‑off debt must include:

- The signed contract or signed application that created the debt, or if none exists, a document provided while the account was active showing the debt was incurred (for revolving credit, the most recent statement with a purchase, payment, or balance transfer is enough).

- The charge‑off account statement (or equivalent) issued by the original creditor.

- A statement describing the complete chain of title from the original creditor to the current owner, including the date of each assignment, sale, or transfer.

- Records of any prior settlement agreement on the debt.

Collectors must also keep evidence of your substantiation request and all documents they sent in response until the debt is discharged, sold, or transferred. These requirements are especially important when junk‑debt buyers sue consumers with incomplete or inaccurate records.

Consumers sued in New York City now have additional documentation protections under the City’s SHIELD Rule, which also sets a 60‑day deadline and limits collection if documentation is not provided.

FDCPA “Verification” vs. New York “Substantiation”

Federal law and New York law use different concepts: verification under the FDCPA and substantiation under New York’s DFS regulations.

Under the FDCPA (15 U.S.C. § 1692g):

- The collector must send a written “validation notice” with basic details: amount of the debt, name of the creditor, and a 30‑day dispute window.

- If you dispute in writing within 30 days, collection must stop until the collector “obtains verification of the debt … or a copy of a judgment” and mails it to you.

- The statute does not define verification in detail and does not impose a specific deadline for how quickly verification must be mailed.

By contrast, New York’s substantiation standard is:

- Available any time during the collection process, not just within 30 days of the first letter.

- Triggered by either oral or written disputes, with duties on the collector to tell you how to request substantiation.

- Tied to a firm 60‑day deadline to provide detailed documentation, with a mandatory halt to collection until substantiation is delivered.

New York’s rules extend well beyond the FDCPA because they specify the documents required, impose clear timeframes, and require cessation of collection where substantiation is lacking. In practical terms, substantiation gives New York consumers a stronger tool to challenge bad records and defend debt collection lawsuits.

If you are being contacted or have been sued by a debt collector in New York, you should consider promptly disputing the debt in writing and requesting substantiation under 23 NYCRR 1.4, in addition to asserting your FDCPA rights. Because the interplay between state regulations, federal law, and court procedures can be complex, speaking with an experienced New York consumer lawyer can help you use these protections effectively.

To discuss a New York debt collection lawsuit or how to use these substantiation rights in your case, you can contact The Law Offices of Robert J. Nahoum, PC through https://nahoumlaw.com.

The Law Offices of Robert J. Nahoum, P.C. represents New York consumers who are sued by debt collectors and who are facing judgment enforcement, including wage garnishments and bank restraints. You can learn more about our consumer protection and judgment enforcement practice and request a free consultation at https://www.nahoumlaw.com.

If you have been contacted by a debt collector contact us at (845) 232‑0202 to discuss your options.

Disclaimer: This blog post is for informational purposes only and does not constitute legal advice. Every case is different; you should speak with an attorney about your specific situation before making legal decisions.