By: Robert J. Nahoum

Receiving an information subpoena after a debt collector wins a judgment against you can be stressful, but knowing your rights and obligations under New York law helps you respond wisely. Below, The Law Offices of Robert J. Nahoum, PC answers the most common questions judgment debtors ask about these subpoenas. If you need personalized help with consumer debt defense, contact us today.

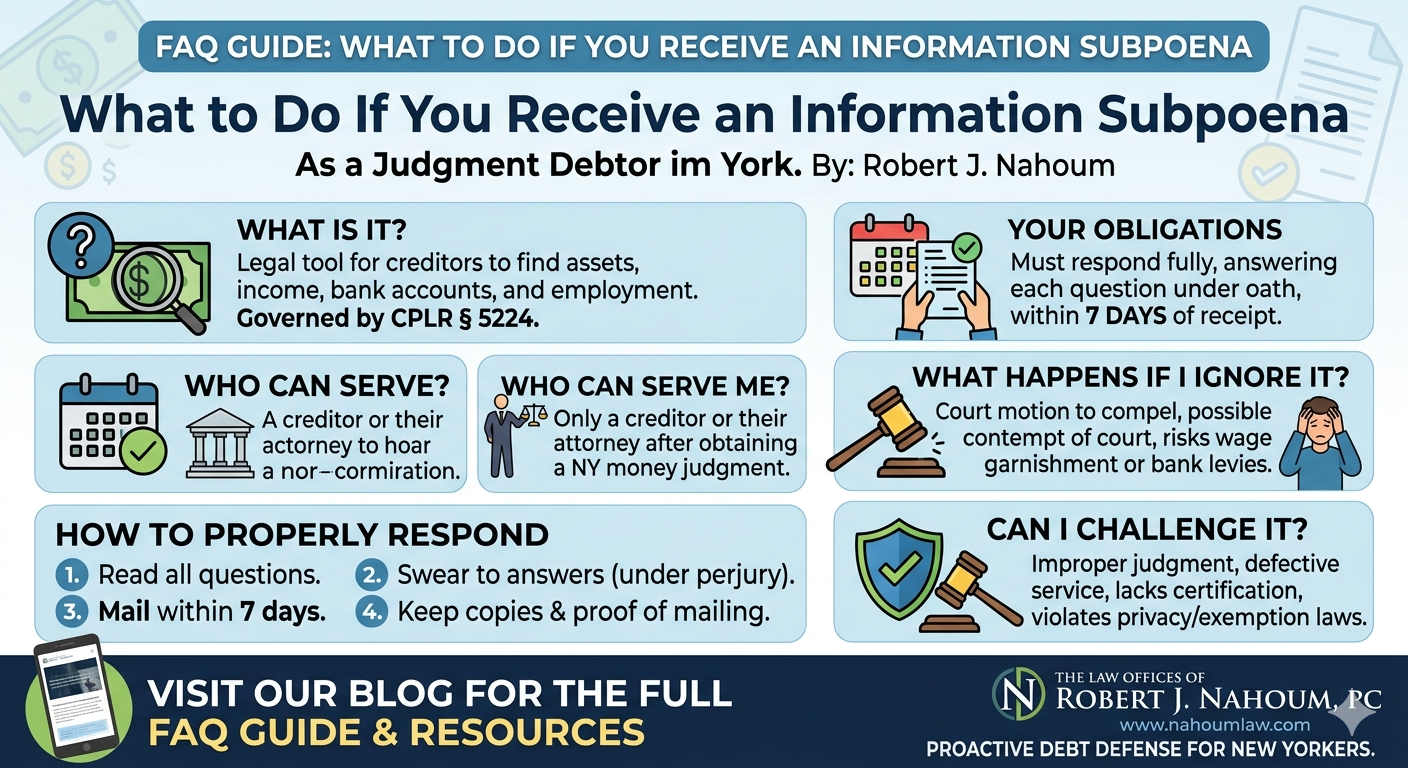

What Is an Information Subpoena?

An information subpoena is a legal tool judgment creditors use after obtaining a money judgment to discover your assets, income, bank accounts, employment, and other financial details for collection purposes. Governed by CPLR § 5224, it can be served on you (the judgment debtor) or third parties like banks, employers, or landlords who might know about your finances. For more on how judgments lead to collection tactics, see our debt collection defense resources.

Who Can Serve Me With One?

Only a creditor (judgment holder) or their attorney can issue an information subpoena once they have a valid New York money judgment against you. Subpoenas to third parties require a certification stating the creditor reasonably believes that person has information about your assets, without it, the subpoena is void. Learn more about challenging improper creditor actions on our legal debt defense page.

What Are My Obligations If I Receive One?

You must respond fully, separately answering each question under oath within 7 days of receipt. No fee is required from judgment debtors, and creditors often include a prepaid return envelope. Answers must be complete, truthful, and mailed to the address specified (usually via registered or certified mail). Failure to comply can escalate collection efforts—read our guide on protecting your rights as a judgment debtor for strategies.

What Happens If I Ignore It?

Ignoring an information subpoena risks serious consequences, including:

- A court motion to compel your compliance

- Contempt of court findings

Courts take these subpoenas seriously, non-response signals evasion and can lead to wage garnishment or bank levies. See how we fight aggressive debt collection to protect clients from these outcomes.

How Do I Properly Respond?

Follow these steps to respond correctly:

- Read every question carefully—answer each one separately and completely.

- Swear to your answers under penalty of perjury (the form includes an affidavit section).

- Mail your response within 7 days using the method specified (often registered mail).

- Keep copies of your answers and proof of mailing for your records.

Partial, evasive, or late answers can be treated as non-compliance. If you’re unsure how to answer without exposing exempt assets, schedule a consultation with our team.

Can I Refuse to Answer Certain Questions?

You may object to questions that are:

- Irrelevant to asset discovery

- Protected by privilege (e.g., attorney-client communications)

- Overly broad or harassing

However, blanket refusals are risky, consult an attorney before withholding information. Valid exemptions (like certain public benefits, Social Security, or protected wages) may apply, but you still must disclose them. Explore our consumer protection services to learn about your exemptions.

How Often Can a Creditor Send Me an Information Subpoena?

Creditors can re-serve information subpoenas anytime until the judgment is fully satisfied (paid off), typically every few months to track new assets or income. This makes proactive debt defense crucial to limit repeated harassment. Read our blog for updates on stopping cyclical collection tactics.

What Defenses or Challenges Are Available?

You may challenge an information subpoena if:

- The underlying judgment was improperly obtained or already satisfied

- Service was defective (e.g., not delivered correctly)

- The subpoena lacks required certifications (for third parties)

- Questions violate privacy or exemption laws

An experienced debt defense attorney can file motions to quash, limit, or vacate improper subpoenas or judgments. At Nahoum Law, we’ve successfully vacated default judgments and stopped unlawful collection for countless clients.

Should I Hire a Lawyer?

Yes, especially if:

- You’re unsure how to answer without self-incrimination

- The judgment is disputed, expired, or incorrectly calculated

- You face wage garnishment, bank levies, or repeated subpoenas

- You want to negotiate a settlement or payment plan

At The Law Offices of Robert J. Nahoum, PC, we protect New York judgment debtors from aggressive collection tactics. Visit our debt collection defense page or contact us to discuss your case today.

Where Can I Learn More?

- Nahoum Law: Consumer Debt Defense

- Nahoum Law: Debt Collection Defense

- Nahoum Law Blog: Legal Insights

- Contact Our Office

Disclaimer: This FAQ is for informational purposes only and does not constitute legal advice. Laws change, and every case is unique—consult a qualified New York attorney at Nahoum Law for guidance on your specific situation.