By: Robert J. Nahoum

Debt collectors increasingly use email and text messages to pursue unpaid debts, but federal law, the Fair Debt Collection Practices Act (FDCPA), sets strict limits on this contact. In New York, these federal protections apply alongside state consumer laws. If a collector is bombarding you with texts or emails, you have rights to push back.

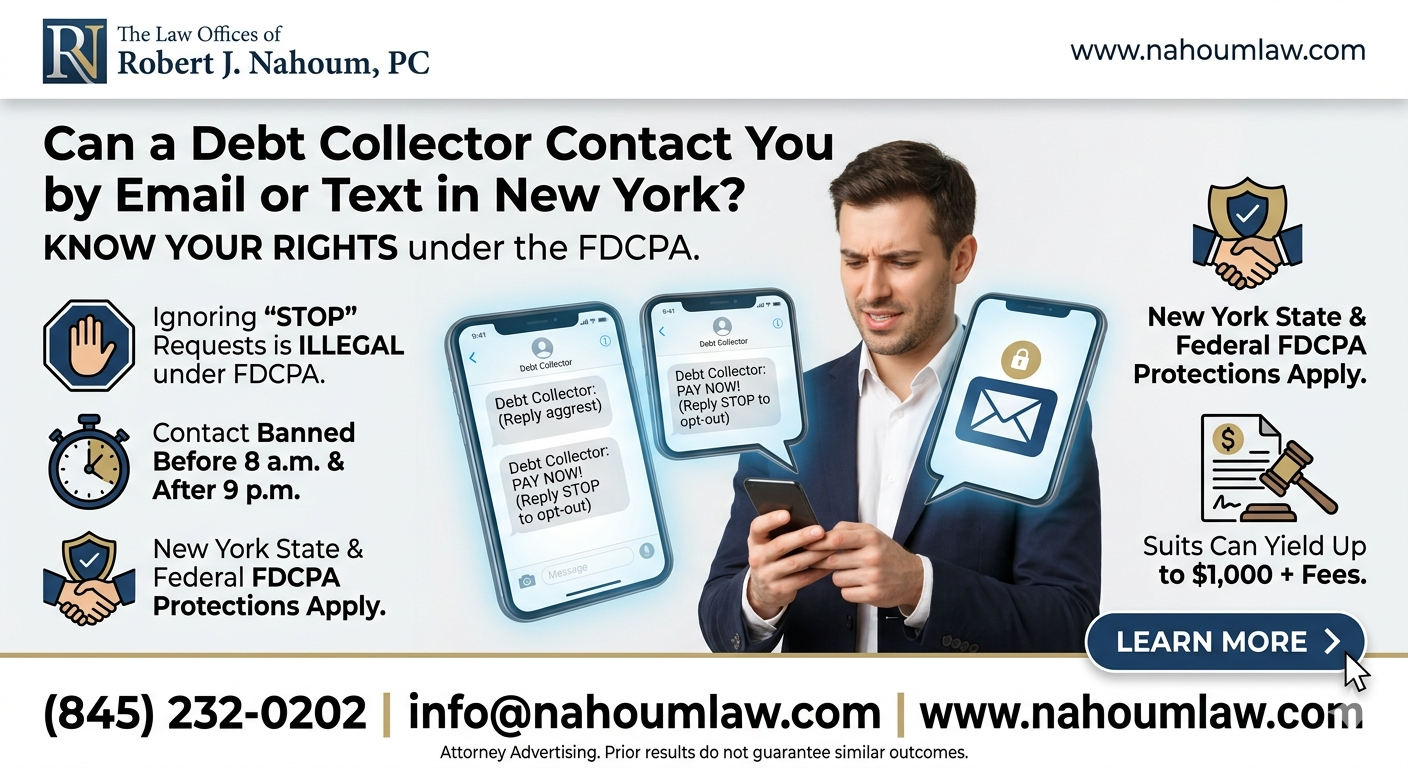

What the FDCPA Says About Debt Collector Contact

The FDCPA is the primary federal law regulating third-party debt collectors, prohibiting harassment, deception, and unfair practices. The law explicitly allows email and text messages as communication methods, provided collectors include clear opt-out instructions and required disclosures in every message. However, the FDCPA bans contact at inconvenient times (before 8 a.m. or after 9 p.m.), to your workplace if known, or after you request they stop.

New York consumers benefit from these FDCPA safeguards, which override any blanket permission for unlimited digital contact.

When FDCPA Permits Email or Text Messages

Under FDCPA regulations updated in 2020, debt collectors may use email or text if:

- You provided the contact information, or they have a reasonable belief it’s accurate.

- Messages identify the collector and include opt-out options (e.g., “Reply STOP to unsubscribe”).

- They avoid work emails or numbers if aware of their professional nature.

Even compliant messages cannot threaten illegal actions like arrest or wage garnishment without a court order.

FDCPA Violations: When Texts or Emails Become Illegal

Repeated, aggressive, or deceptive electronic contact often violates the FDCPA. Common red flags include:

- Ignoring your “stop” request.

- Sending messages that harass, abuse, or falsely threaten lawsuits.

- Revealing your debt to third parties (e.g., via public social media).

- Contacting you after you’ve disputed the debt in writing.

New York courts aggressively enforce FDCPA claims, often awarding statutory damages up to $1,000 per violation, plus attorney fees.

Steps to Protect Yourself Under the FDCPA

Follow these actions if facing unwanted debt collector emails or texts:

- Document everything—screenshot messages with dates, times, and sender details.

- Request cessation in writing—send a certified letter invoking your FDCPA right to stop contact (except to confirm cessation or notify of lawsuits).

- Dispute the debt—within 30 days of initial contact, demand validation under the FDCPA.

- Avoid engaging verbally—limit responses to written disputes.

Preserving evidence strengthens potential FDCPA lawsuits.

FAQ: Debt Collector Email/Text Rights in New York

Can debt collectors text me under the FDCPA?

Yes, but only with opt-out notices and without harassment; repeated ignored “stop” requests violate the FDCPA.

Does the FDCPA allow work emails from collectors?

No—collectors must avoid known workplace contact to prevent embarrassment or interference.

What if a debt collector ignores my cease communication letter?

Continued contact breaches FDCPA Section 805(c), opening claims for damages.

Can I sue for FDCPA violations from texts/emails?

Yes—file within one year; successful suits yield up to $1,000 plus fees, no actual harm required.

How does New York law interact with FDCPA email rules?

State laws enhance FDCPA protections, especially against deception or old debt revival.

Contact Nahoum Law for FDCPA Help

Facing FDCPA violations from aggressive texts or emails? Nahoum Law specializes in consumer debt defense. Visit our debt collection harassment page or contact us for a free consultation. Read more on FDCPA rights and protect your rights today.

If you need help settling or defending a debt collection lawsuit, stopping harassing debt collectors or suing a debt collector, contact us today to see what we can do for you. With office located in the Bronx, Brooklyn and Rockland County, the Law Offices of Robert J. Nahoum defends consumers in debt collection cases throughout the Tristate area including New Jersey.

The Law Offices of Robert J. Nahoum, P.C

(845) 232-0202

www.nahoumlaw.com

info@nahoumlaw.com

Attorney Advertising Disclaimer: This blog post is for general informational purposes only and does not constitute legal advice. Laws vary by state, and outcomes depend on specific facts. Consult an attorney for personalized guidance. Prior results do not guarantee similar outcomes.