By: Robert J. Nahoum

Has Your Bank Account Been Frozen by a Debt Collector?

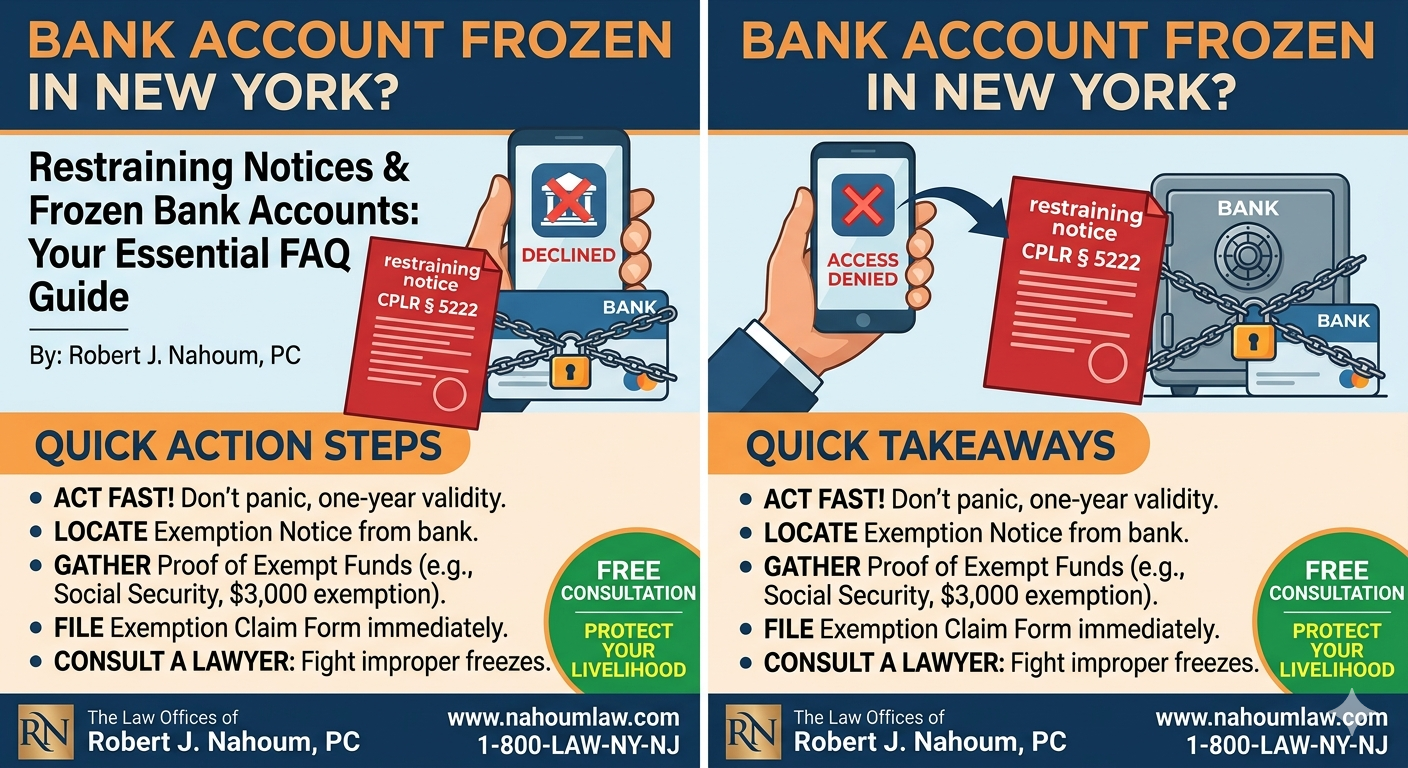

Learning that your bank account is frozen is one of the most stressful financial events a consumer can face. In New York, this is often the result of a Restraining Notice served by a judgment creditor or debt collector. If you are facing this situation, you need immediate, accurate legal information to protect your livelihood.

Frequently Asked Questions About Restraining Notices

- What is a Restraining Notice in New York?

A Restraining Notice is a powerful post-judgment enforcement tool used by creditors under CPLR § 5222. Once a creditor obtains a money judgment against you, they can serve this notice on your bank (or any third party holding your assets).

Upon receipt, the bank is legally required to “freeze” or “restrain” any funds in your account up to double the amount of the judgment. This means you cannot withdraw, transfer, or use the money until the notice is vacated, expires, or the debt is satisfied.

- How Do I Know If My Account Is Frozen?

Often, the first sign is a declined transaction or an inability to access your funds. However, New York law provides specific protections regarding notification:

- Bank’s Duty to Notify: Under CPLR § 5222-a, your bank must mail you an Exemption Notice and two copies of an Exemption Claim Form within two business days of receiving the restraining notice.

- Check Your Mail: If you haven’t received these forms, contact your bank immediately. Failure to receive proper notice can sometimes be grounds for challenging the enforcement.

If you suspect a freeze but haven’t received paperwork, do not wait. Time is critical. Learn more about our Debt Collection Defense services.

- Is Any Money in My Account Protected (Exempt)?

Yes. New York law recognizes that freezing an account can leave a debtor unable to pay for basic necessities. Certain funds are legally exempt from restraint:

- The $3,000 Exemption: The first $3,000 in your bank account is generally exempt from restraint. If your balance is below this threshold at the time of service, the restraining notice should not effectively freeze your funds.

- Protected Benefit Funds: Funds derived from specific government benefits are often 100% exempt, including:

- Social Security (SSI/SSDI)

- Veterans Benefits

- Child Support and Spousal Maintenance

- Unemployment Insurance

- Workers’ Compensation

- Public Assistance (welfare).

Crucial Point: These funds do not automatically become available; you often must prove their exempt status using the Exemption Claim Form provided by your bank.

- What Should I Do Immediately If My Account Is Frozen?

If a debt collector has frozen your account, take these emergency steps:

- Do Not Panic, But Act Fast: A restraining notice is valid for one year and can be renewed. Delaying can result in a marshal levying (taking) your funds.

- Locate the Exemption Notice: Find the forms mailed by your bank. If you didn’t receive them, request them immediately.

- Gather Proof of Exemptions: Collect bank statements, award letters, or direct deposit records showing that the frozen funds come from exempt sources (e.g., Social Security).

- File Your Exemption Claim: Complete and return the Exemption Claim Form to the bank and the creditor’s attorney promptly.

- Contact an Attorney: If the debt is disputed, the judgment was entered by default without proper service, or the amount is significant, you may need to file an Emergency Motion to Vacate the judgment or the restraining notice.

For immediate assistance, visit our page on Consumer Protection or contact our office today.

- Can a Restraining Notice Be Challenged or Vacated?

Absolutely. A restraining notice is only valid if the underlying judgment is valid. Common grounds to challenge the freeze include:

- Improper Service: If you were never properly served with the original lawsuit, the judgment may be void for lack of personal jurisdiction.

- Mistaken Identity: Sometimes banks freeze accounts due to similar names or outdated information.

- Exempt Funds: If the account holds only exempt funds, the restraint may be improper.

- Bankruptcy: Filing for bankruptcy triggers an Automatic Stay, which immediately stops collection efforts and can help avoid the lien on your account.

Our firm has extensive experience filing motions under to vacate default judgments and release frozen assets.

- How Long Does a Restraining Notice Last?

In New York, a restraining notice served on a bank is valid for one year from the date of service. However, creditors can renew it indefinitely if they act before it expires. This is why resolving the underlying debt or vacating the judgment is essential to permanently unfreeze your account.

Why Choose The Law Offices of Robert J. Nahoum, PC?

Debt collection laws are complex, and banks often err on the side of the creditor. You need an advocate who understands both the Fair Debt Collection Practices Act (FDCPA) and New York’s CPLR enforcement statutes.

Robert J. Nahoum is a seasoned consumer protection advocate with over two decades of litigation experience in New York and New Jersey. We have successfully helped countless consumers:

- Unfreeze bank accounts containing exempt funds.

- Vacate improper default judgments.

- Defend against aggressive debt collection lawsuits.

Get Your Free Consultation Today

If your bank account has been frozen by a restraining notice, do not wait for the money to be levied. Contact The Law Offices of Robert J. Nahoum, PC immediately.

📞 Call Us: [Insert Phone Number]

📍 Serving: all of New York State

🌐 Learn More: www.nahoumlaw.com

Disclaimer: This blog post is for informational purposes only and does not constitute legal advice. Laws change frequently, and every case is unique. Please consult with an attorney regarding your specific situation.