By: Robert J. Nahoum

What Is Wage Garnishment in a Debt Collection Case?

Wage garnishment (called an “income execution” in New York) is a post-judgment remedy where a debt collector takes money directly from your paycheck to satisfy a court judgment obtained in a consumer debt lawsuit. Unlike tax agencies or child support enforcement, private debt collectors must first sue you, win a lawsuit, and obtain a money judgment before they can garnish your wages in New York.

If you never received court papers, never appeared in court, or never agreed to the debt, you may have powerful defenses to stop the garnishment entirely.

How Much of My Wages Can a Debt Collector Garnish?

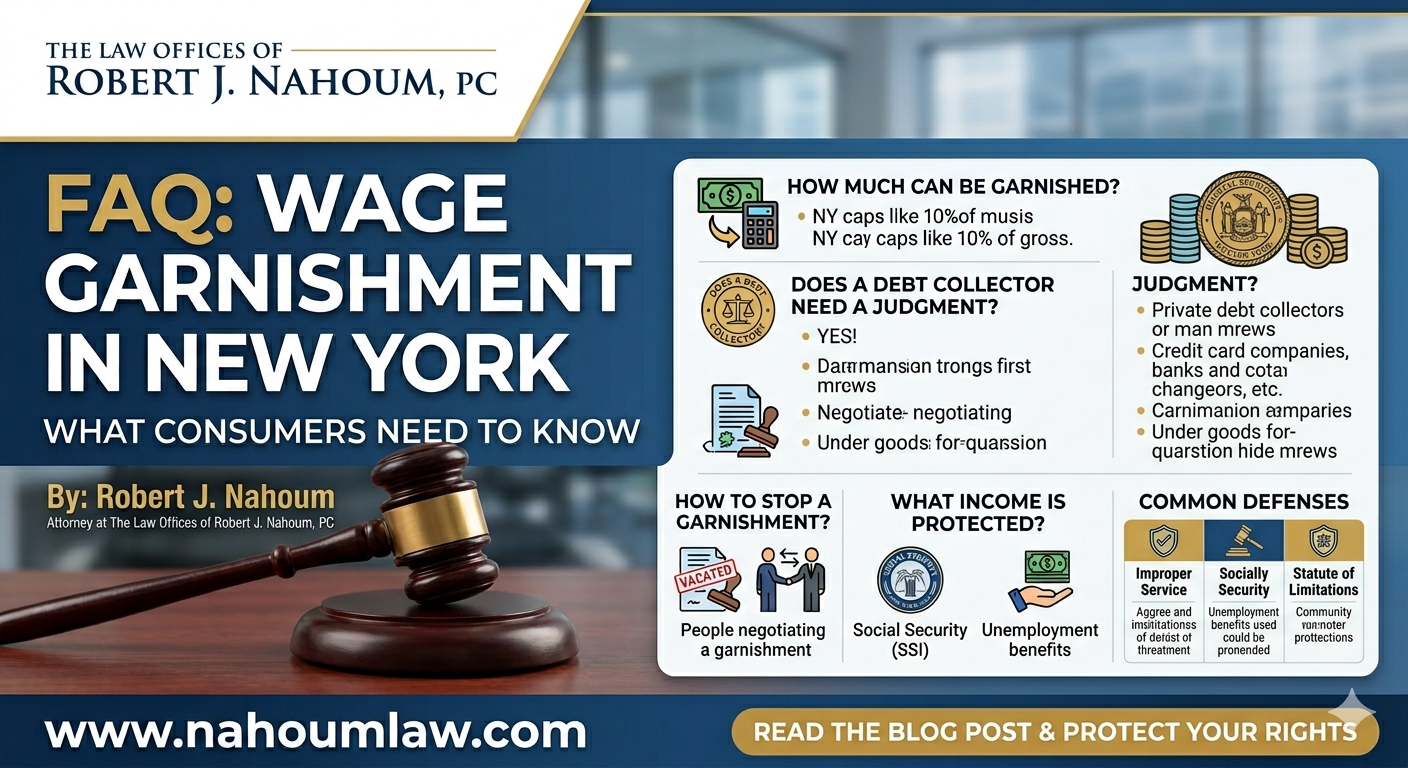

New York law offers stronger protections than federal law for consumers facing debt collection garnishments. A judgment creditor (such as a credit card company, debt buyer, or auto lender) can garnish the lesser of:

- 10% of your gross wages, or

- 25% of your disposable income (what’s left after mandatory deductions like taxes and Social Security) to the extent it exceeds 30 times the federal or state minimum wage (whichever is greater).

If your disposable income is less than 30 times the minimum wage, it cannot be garnished at all.

Example: If you earn $1,000 per week gross, the maximum a debt collector can take is $100 (10%), not $250 (25%).

Do Debt Collectors Need a Court Judgment to Garnish My Wages?

Yes, absolutely. In New York, private debt collectors, including credit card companies, banks, junk debt buyers, and auto deficiency lenders, must sue you and obtain a court judgment before issuing an income execution.

If a debt collector is threatening to garnish your wages without having sued you or obtained a judgment, they are likely violating the Fair Debt Collection Practices Act (FDCPA) and New York debt collection laws.

Can My Employer Fire Me for a Debt Collection Garnishment?

No. Under the federal Consumer Credit Protection Act (CCPA), your employer cannot fire you solely because your wages are being garnished for one debt collection judgment. However, this protection may not apply if you have garnishments for two or more separate debts.

How Do I Stop a Wage Garnishment from a Debt Collector?

You have several legal options to stop or reduce a wage garnishment stemming from a debt collection lawsuit:

- Vacate the Underlying Judgment

If you were never properly served with the lawsuit (improper service), if the debt is time-barred, if the debt isn’t yours, or if the collector lacks standing to sue, you may be able to vacate (undo) the judgment entirely. Once the judgment is vacated, the garnishment must stop. This is often the most powerful defense and requires experienced legal representation.

- File an Exemption Claim (Hardship Hearing)

If the garnishment causes extreme financial hardship, leaving you unable to pay for basic necessities like rent, food, or utilities, you may file a claim of exemption with the court. A judge can reduce or eliminate the garnishment if your income is below protected levels or if the garnishment creates undue hardship.

- Negotiate a Settlement

Contact the debt collector’s attorney to negotiate a voluntary payment plan or lump-sum settlement. If accepted, they may withdraw the income execution and release the garnishment.

- File for Bankruptcy

Filing Chapter 7 or Chapter 13 bankruptcy triggers an automatic stay, which immediately stops wage garnishments for consumer debts like credit cards, medical bills, personal loans, and auto deficiencies. Bankruptcy may also discharge (eliminate) the underlying debt entirely, ending the garnishment permanently.

What Types of Income Are Protected from Debt Collection Garnishment?

New York law protects certain types of income from garnishment by private debt collectors, including:

- Social Security benefits

- Supplemental Security Income (SSI)

- Veterans’ benefits

- Public assistance (welfare)

- Workers’ compensation

- Unemployment benefits

- Child support received

- Most pension and retirement accounts.

If your paycheck includes any of these protected funds commingled with wages, they may be exempt from garnishment. Debt collectors cannot touch these protected sources even after obtaining a judgment.

Common Defenses to Debt Collection Garnishments

If you’re facing garnishment from a debt collection lawsuit, you may have one or more of these defenses:

| Defense | Description |

| Improper Service | You were never properly served with the summons and complaint, violating your due process rights . |

| Statute of Limitations | The debt is time-barred (typically 6 years for most consumer debts in New York) . |

| Lack of Standing | The debt collector cannot prove it owns the debt or has the right to sue you . |

| Incorrect Amount | The judgment amount includes improper fees, interest, or charges . |

| Identity Theft / Wrong Debtor | The debt belongs to someone else or resulted from identity theft . |

| Already Paid or Discharged | The debt was already paid, settled, or discharged in a prior bankruptcy . |

How Can The Law Offices of Robert J. Nahoum, PC Help?

If you’re facing wage garnishment from a debt collection lawsuit, you have rights—and powerful defenses. At The Law Offices of Robert J. Nahoum, PC, we represent consumers sued by debt collectors throughout New York and New Jersey. We can:

- Review whether the underlying judgment was properly obtained

- Assert defenses like improper service, statute of limitations, or lack of standing

- File motions to vacate default judgments and stop garnishments immediately

- Negotiate with creditors to reduce or eliminate the debt

- Advise on bankruptcy options if appropriate

Visit our Legal Debt Defense page to learn more about how we protect consumers from aggressive debt collection lawsuits and unlawful garnishments.

Frequently Asked Questions

How long does a wage garnishment from a debt collector last in New York?

A garnishment continues until the judgment is paid in full, you negotiate a settlement, you file bankruptcy, or the judgment expires. New York judgments are valid for 20 years and can be renewed, so acting quickly is essential.

Can a debt buyer garnish my wages without suing me?

No. Debt buyers and third-party collectors must sue you, prove their case, and win a judgment before garnishing wages in New York. If they’re threatening garnishment without a lawsuit, they may be violating the FDCPA and state law.

What should I do if I receive an Income Execution notice from a debt collector?

Act immediately. You typically have only a short window (often 20 days) to respond before your employer begins withholding wages. Contact an attorney right away to explore options for vacating the judgment, filing an exemption claim, or negotiating a resolution.

What is the statute of limitations on consumer debt in New York?

For most consumer debts, including credit cards, personal loans, medical bills, and auto deficiencies, the statute of limitations is three years from the date of default or last payment. If a debt is time-barred, the creditor cannot legally sue you, and any judgment based on a time-barred debt may be vacated.

Can I stop a garnishment if I wasn’t properly served with the lawsuit?

Yes. If you were never properly served with the summons and complaint, you may be able to vacate the default judgment and stop the garnishment entirely. This is one of the most common and successful defenses we raise at our firm.

Contact Us Today

Don’t let a debt collector drain your paycheck. If you’ve been sued by a debt collector, received a default judgment, or are facing wage garnishment, call The Law Offices of Robert J. Nahoum, PC today for a consultation. We protect consumers’ rights across New York and New Jersey.

📞 Call us or visit www.nahoumlaw.com to learn more about our consumer protection and debt collection defense services.

Disclaimer: This blog post is for informational purposes only and does not constitute legal advice. Every case is unique. Consult with an attorney to discuss your specific situation and legal options.